Before I started writing in the personal finance space, I spent nearly 8 years working alongside my husband in a funeral home. My husband Greg worked as a mortician, and I was the Director of Family Services. I learned so much about living and dying during my years in the mortuary business, but there’s one that stuck with me — the real-life consequences of not having life insurance.

I clearly remember speaking with dumbfounded families who couldn’t believe their husband or father (or wife or mother) never had life insurance in place. Some didn’t have enough money to cover final expenses like the funeral bill, and others confided in me they had no idea how they would pay their bills.

This saddened me greatly since I know first-hand how inexpensive life insurance can be — especially if you’re young and healthy. After all, I’m a 40-year-old woman and I currently have two term policies worth $1 million dollars that set me back a grand total of $53 per month.

Why People Don’t Buy Life Insurance

The main reason consumers don’t buy this important coverage is simple — they get busy and forget. Most of us know we need life insurance in place during our working years, and that’s especially true for those of us with kids. But it’s easy to let life get in the way, and for the purchase of life insurance to wind up on a list of other to-dos that we never get to.

Not only that, but people don’t want to think about dying. I specifically remember a family I met in the funeral home who just lost a husband and father who wasn’t even 40-years-old. In tears, his wife explained that he had told her he was going to buy life insurance dozens of times, but that he hated even dealing with death. He had a $20,000 life insurance policy through work, and he knew he needed more, but he didn’t want to face his mortality in his free time. Unfortunately, his family paid dearly for that decision.

A final reason people don’t buy life insurance is cost. The thing is, term coverage is so cheap that almost anyone can afford it. People just think it’s expensive, so they shy away from taking the next steps. Life insurance is also just another bill to pay, and many can barely keep up with the bills they have.

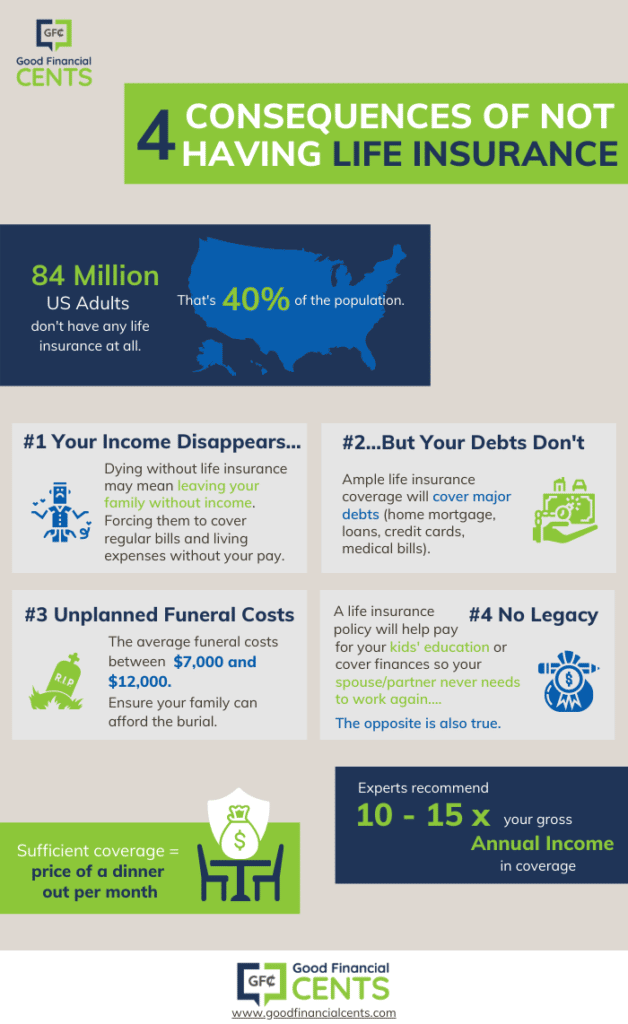

That’s probably why so few people have enough coverage. Here are some statistics that should scare you:

- Only around 60 percent of Americans had life insurance in 2022, according to LIMRA’s 2022 Insurance Barometer Study

- Among those with life insurance, 1 in 5 people know they do not have enough

- Consumers surveyed tend to overprice life insurance; millennials in particular believe that life insurance costs 5x the actual amount for a policy

Consequences of Not Having Life Insurance

Based on those statistics, not enough people have life insurance and those who do may not have enough coverage to last. But, what can this mean for your family? Here are the main downsides you’ll face when you don’t buy life insurance now, before it’s too late:

Your Income Disappears

Income replacement is one of the most compelling reasons to buy life insurance, and that’s especially true if you have kids. You don’t want your income to suddenly disappear, leaving your family in the lurch. However, this is exactly what happens when you die without life insurance. All of a sudden, your family is left trying to cover regular bills and living expenses without your income.

That’s why many experts suggest buying at least 10x your income in term life insurance coverage. This way, your family will have some cash they can use to replace your income while they mourn and get back on their feet.

Your Debts Don’t

Your income may disappear when you die, but your debts certainly don’t. With that in mind, you should buy life insurance coverage that will cover major debts you have like your home mortgage, your family car loans, and any credit card debt you have.

If you don’t buy life insurance and you die before your time, your family will be left trying to cover all your debts without your help. It’s shameful to leave them in this position — especially when term life insurance coverage can easily be purchased for the price of a dinner out per month.

Your Family Could Need a GoFundMe to Pay for Your Funeral

During my final years in the funeral industry, GoFundMe came about. I cannot tell you how many families came in to plan their services without any money only to find that, no, the funeral home wouldn’t let them make payments. After that, they’d set up a GoFundMe and solicit donations from family and friends to pay for a service.

This always made me sad, mostly because families shouldn’t have to struggle or fundraise to pay for final expenses. I always thought that, if only their loved one had a small term life insurance policy, they would have been able to grieve without the added stress.

You Will Not Leave a Legacy

Finally, life insurance offers you the chance to leave a legacy behind. This could mean leaving enough money to pay for college tuition for your children, or having a broad enough policy so your spouse or partner never needs to work again, paving the way for them to stay home and nurture your kids. When you have enough life insurance so your family is taken care of, they will never forget it.

The opposite is also true. Many whose loved ones die without life insurance wind up angry and resentful at their partner for leaving them in such a position. I know because I saw it with my own eyes, and I felt their exasperation as they tried to figure out what to do.

Purchase Life Insurance the Painless Way

Here’s the thing: Buying life insurance doesn’t have to be complicated or stressful. I know because I have purchased $1 million in life insurance coverage, and because the second policy I bought online didn’t even require a medical exam.

The purchase of life insurance can be painless and fast if you plan to buy basic term coverage, and it can also be significantly cheaper than you think it would be. These tips can help you get the coverage you need without any added hassle or stress.

1. Shop Around and Compare Quotes Online

First, you should absolutely shop around and compare life insurance quotes online, mostly because this is such an easy task. A range of online life insurance providers including Haven Life and Bestow make it easy to price out a policy in a matter of minutes online.

To get a quote from Bestow or Haven Life, for example, all you need to supply is your birth date, your height, your weight, and your zip code. You don’t even need to enter your contact information or your email to get a free quote with either company.

You can also check out our guide to the Best Life Insurance Companies of 2023, which lets you read reviews of all the top providers and compare rates from multiple providers in one place.

Whatever you do, don’t go with the first life insurance company you come across. Make sure you compare policies in terms of their monthly cost, the amount of coverage, and how long it lasts. Then, and only then, can you know you’re getting the best deal.

2. Play Around with Coverage Amounts

You also need to have a general idea of how much coverage you want and need. We mentioned that most experts suggest buying at least 10x your income in life insurance coverage, but it may be prudent to buy more term coverage than you need. After all, there’s no such thing as having too much life insurance in place, but you can definitely not have enough.

You’ll also want to decide how long you want your policy to last. Most term life insurance policies last for 10, 15, 20, or 30 years, letting you tailor your policy to your needs.

If you’re young and you have young kids, you may want a 30-year policy that will provide income replacement for your entire working life. If you’re in your 40’s and you plan to retire at 55, on the other hand, you may feel comfortable with a policy that lasts for 15 or 20 years. There is no “right” or “wrong” answer, but these are factors you should consider.

3. Look for Providers that Don’t Require a Medical Exam

According to LIMRA’s 2018 Insurance Barometer Study, half of all consumers say they are “more likely to purchase life insurance if priced without a physical examination.” And, can you blame them? Medical exams require a blood draw, and you have to set aside time in your schedule for them to boot. It’s easy to procrastinate and never buy a policy when a medical exam is required.

Fortunately, many life insurance providers don’t require a medical exam. Instead, they rely on algorithms to determine who is the greatest risk, and who can purchase coverage that begins right away. The second policy I purchased for myself came from Haven Life, and it did not require a medical exam.

I was in my late 30’s when I purchased this policy for $750,000, and I only pay around $27 per month. I applied for this policy online and had coverage the next day, and all without seeing a nurse or facing the dreaded needle prick.

The Bottom Line

Since you took the time to read this piece, you are probably on the verge of buying life insurance. You already know you need it, so don’t let another day go buy without coverage. You may not think something could happen to you in the next week or the next few months, but life doesn’t always go as planned. If you’re unlucky, your untimely death may be no exception.

Take the time to get a quote for life insurance, and you’ll never have to wonder what your family would do if you died. Life insurance lets you continue providing for them even after you’ve left this Earth, and there’s nothing more thoughtful and loving than that.