Today’s modern family is not just a product of biology.

Ontario’s Children’s Law Reform Act gives special status to a person who has “formed a settled intention to treat the child as a child of his or her own family,” the judge said.Photo by Getty Images/iStockphoto

Reviews and recommendations are unbiased and products are independently selected. Postmedia may earn an affiliate commission from purchases made through links on this page.

Article content

Today’s modern family takes its shape in many ways. And a whole new set of family law questions emerge when single parents form new relationships, because step-parents and stepchildren are born. What happens if the parents in the blended family separate? Does a step-parent have a right to spend time with their stepchild even though the parents’ relationship has ended?

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

Article content

That question was recently before Justice Margaret Eberhard of Ontario’s Superior Court of Justice. In the case, a single mother of a one-year-old daughter met her new partner in July 2018 and the couple began living together one month later. The new partner did not have any children of his own. Three years later, the relationship ended. Shortly thereafter, the stepfather requested parenting time with his stepdaughter, which the mother refused. In early October, the parties made their way to the courtroom to resolve the dispute.

Financial Post Top Stories

Sign up to receive the daily top stories from the Financial Post, a division of Postmedia Network Inc.

By clicking on the sign up button you consent to receive the above newsletter from Postmedia Network Inc. You may unsubscribe any time by clicking on the unsubscribe link at the bottom of our emails. Postmedia Network Inc. | 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Financial Post Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

During the relationship, the stepfather said he and the daughter shared a close bond, despite the relative brevity of the parties’ relationship. Since the daughter never had a relationship with her biological father, the new partner quickly became a father figure. According to the stepfather, he was involved in all aspects of the daughter’s care and the daughter almost always called him “Daddy.”

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

The mother’s view of the stepfather’s relationship with the daughter was almost completely at odds with the stepfather’s account. According to the mother, she was always primarily responsible for the care of the daughter and made all important decisions for her, such as choice of daycare and medical treatment. The mother said the daughter called the stepfather by his first name and only “occasionally called him Dad.”

The judge accepted the stepfather’s evidence and rejected the mother’s, describing the evidence as “beyond challenge” that the mother and stepfather “both participated fully in parenting the child.” The judge found there had been “no distinction drawn by reason of the (stepfather) not being the biological father” and that the mother “proclaimed and encouraged (the stepfather’s) excellence in being a parent.”

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

From there, the judge went on to apply the law. To start, the judge framed the question she was being asked: What is the mother’s autonomy to raise her child as she sees fit, without the stepfather’s involvement?

In support of her argument that the stepfather should not have any parenting time, the mother pointed to a long line of court decisions dealing with a grandparent’s right to spend time with a grandchild. The judge made clear the case before her was different. The difference is rooted in Ontario’s Children’s Law Reform Act, which gives special status to a person who has “formed a settled intention to treat the child as a child of his or her own family.” For the judge, there was no doubt the stepfather had that special status.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

The stepfather’s special status was not determinative, however. The child’s best interests always have priority. According to the judge, a determination of best interests may include factors such as “length of the relationship, the age and developmental stage of the child during the relationship and when contact ceased, the length of time since contact ceased, and the extent of the step-parent’s participation in usual parenting imperatives.”

In the result, the stepfather was granted parenting time with his stepdaughter.

One of the challenges the judge faced in making the order for parenting time was that nine months had gone by after the parties’ separation. Since the daughter had little, if any, contact with her stepfather during that time, there was concern the daughter could experience distress from the sudden reintroduction of the stepfather. The judge acknowledged that nine months was a significant gap for a young child.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

“There is likely an inherent loss of the child’s perception of the (stepfather) and her relationship with him due to that passage of time which could be said to raise a risk in resumption,” the judge said. However, in this case, the real risk was the one “taken by the (mother) when she abruptly and unilaterally terminated an ongoing, committed, step-parent/child relationship.”

In addition to his request for parenting time with his stepdaughter, the stepfather requested an “order that he be permitted to pay” child support. Since he will have parenting time with his stepdaughter, the stepfather now pays child support to the mother.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

While secondary to the main issue in the case, the mother’s position created a risk that she would have to pay the stepfather’s legal costs in the event he was granted parenting time. Given his success, the stepfather sought costs from the mother in the amount of $26,570.27. The mother resisted on the basis that an order for costs would negatively impact her ability to care for the child. The judge disagreed and ordered the mother to pay costs of $20,000 to the stepfather.

In the end, today’s modern family is not just a product of biology. Rather, it is constituted in many different ways. Regardless of the process of its formation, a child’s best interests remain paramount when parents, or stepparents, separate.

Adam Black is a partner in the family law group at Torkin Manes LLP in Toronto. [email protected]

Share this article in your social network

Advertisement

This advertisement has not loaded yet, but your article continues below.

The very thought of getting into real estate investing can be overwhelming. There’s a lot of work involved in finding the right property, not to mention the many expenses involved with purchasing real estate. On top of this, you have to worry about finding good tenants and being a landlord.

You can avoid the hassle and the expense by joining one or more real estate investment apps. Just download the app on your phone and invest a few dollars(or more). These crowdfunded real estate platforms are available for every possible situation and financial level, so you can begin right now even if you don’t have the funds for a traditional downpayment.

New real estate investment apps are constantly popping up, so you don’t have to worry about finding the right platform for your financial situation and level of expertise. To help, I’ve compiled the following list of the best real estate investing apps.

Best Real Estate Investing Apps

Roofstock: Best Overall

Arrived Homes: Best for Rental Properties

Fundrise: Best for Beginners

RealtyMogul: Best for REITs

CrowdStreet: Best for Commercial Real Estate

Acretrader: Best for Farmland

Groundfloor: Best for High Liquidity

Yieldstreet: Best for Alternative investments

HappyNest: Best for Simplicity

1. Roofstock

Best Overall

Roofstock lets you invest in rental properties without leaving your home. Its primary service is a marketplace where you can purchase and sell single-family rental properties. Roofstock’s marketplace is free to use so that anyone can search through the different properties offered.

You can uncover all of the information that you need before investing the single-family units, such as

Newly listed units

Neighborhood ratings

Local schools

Pre-inspection information

Yield options

Roofstock is one of the most popular investing apps – they’ve already passed over $5 billion in transactions in more than 70 real estate markets. You can read our full Roofstock review for more information.

2. Arrived Homes

Best for Rental Properties

If you’re looking for a simple real estate investing app, you will want to check out Arrived Homes. With this app, you can purchase shares of vacation rentals for as little as $100. As an investor in Arrived Homes, you don’t have to worry about vetting properties, finding tenants, screening guests, or any paperwork involved in purchasing or renting real estate. Instead, you can collect your rental income share quarterly without getting off the couch.

According to Arrived Homes, you can invest in shares of vacation rentals, currently a booming rental market. The website mentions how a permanent vacation rental can bring up to 130% more revenue than a traditional long-term property. The US vacation rental market is also expected to reach $20 billion by 2025.

You earn money with Arrived Homes through passive income and appreciation. The investment team vets every property to ensure it’s up to standards. The company has funded over 190 properties already, charging a 1% asset management fee plus an 8% property management fee and variable sourcing fees.

If you’re looking to test the waters with real estate investing apps, you can start here until becoming more comfortable.

3. Fundrise

Best for Beginners

Fundrise prides itself on combining investing expertise with technology to bring investment funds to the 371,000-plus investors on the platform. While many of these opportunities would historically be designated for billion-dollar institutions, you can access them from the comfort of your couch.

Many experts consider Fundrise the best real estate investing app for beginners because you can get started without allocating a significant portion of your savings.

With Fundrise, you can also be a hands-off real estate investor since you don’t have to worry about screening tenants or trying to fix up a place.

Here are some of the main perks of using Fundrise:

You can get started for as little as $10 without worrying about saving up for a downpayment.

There are many options for non-accredited investors.

You get many offerings and can go through multiple options until you find the right property.

It has a simple fee structure. Since investing in real estate often comes with a plethora of surprise expenses, it’s a game change to have a platform with a transparent fee schedule.

RealtyMogul invests in commercial properties to help members finance well-leased properties. It presents the opportunity to invest in REITs to generate passive income.

RealtyMogul has two private REITs for investors that aren’t accredited and additional private real estate investments for accredited investors. The minimum to getting started on the platform is $5,000.

With over 250,000 investors and over $950 million invested on the platform, RealtyMogul has granted exposure to about $5.7 billion in deals. With a wide variety of properties, it’s no secret why this is becoming one of the most user-friendly platforms for real estate investing. Learn more in our RealtyMogul review.

5. CrowdStreet

Best for Commercial Real Estate

If you’re looking for something completely different from the other real estate investing apps on this list, consider CrowdStreet. This app allows accredited investors to include commercial real estate projects in their portfolios.

The minimum investment will vary on every project, but you need at least $25,000 in most cases. You can invest in direct deals on the CrowdStreet marketplace or purchase shares of commercial REITs if that’s what you’re looking for.

CrowdStreet can also work with you in an advisory role so that you have a team that helps you optimize your real estate portfolio with the right deals based on your financial commitment.

As of October 2022, CrowdStreet has over 709 deals funded with $4 billion invested. They don’t charge any account fees to investors, and more options are available to qualified investors looking to get serious about building a real estate portfolio.

6. AcreTrader

Best for Farmland

AcreTrader allows you to invest in actual farmland, with various options nationwide, from North Carolina to California. AcreTrader vets every farm before listing it so you can trust the property listing. You don’t have to do anything, as AcreTrader management handles everything from insurance to working with local farmers.

They list about one to two new farms new week, and each listing includes the minimum investment required. One of the recently-listed farms was in Dawson County, Nebraska, with a minimum investment of $10,740 and a specialization in corn and soybeans.

Before investing, you can access all the information you want about the farm. Here’s some of the information that AcreTrader shares:

Description of the land

A map of the surrounding area

Financials and investment highlights

The photos and documents needed to make an informed investment decision

How can you make money with AcreTrader? The company distributes excess annual income to investors with a yield of 3-5% for the lower-risk properties. AcreTrader also makes money for its investors through land appreciation. When the land is sold, you’ll receive your principal and any appreciation accrued when you held the farmland.

To invest with AcreTrader, you must be an accredited investor willing to keep an illiquid property, meaning you’ll need to hold it for at least 5-10 years. You could also sell your shares through the AcreTrader platform if you would like to exit earlier than that. Check out our full review of AcreTrader for more information.

7. Groundfloor

Best for High Liquidity

Groundfloor touts that you can get into “savesting” since it combines saving with investing. The company even promises an annual rate of return of 10%, much more than we’ve seen in most other apps. Plus, tangible assets secure your investment in Groundfloor.

How can you use Groundfloor as a real estate investing app?

You can decide on individual renovation loans that you want to invest in.

You can use automatic investing tools to keep funding projects that match your preferred criteria.

On average, Groundfloor repays investments every 4-12 months – it’s rare to find such liquidity in a secured investment backed by tangible assets.

You can also take advantage of the savings account offered by Groundfloor. The Stairs product allows you to earn 4% interest on your money with no account minimums, the ability to withdraw at any time, and it’s free to use.

With roughly 200,000 users and over $240 million in assets under management, you can trust your money with Groundfloor.

8. Yieldstreet

Best for Alternative Investments

Yieldstreet is an alternative investment that gives retail investors inside access to unique asset classes traditionally dominated by hedge funds and the wealthy. The private investments can range from multi-family rental properties to expensive art.

Investors without accreditation can invest in Yieldstreet’s Prism Fund for $2,500, while accredited investors can build a custom portfolio for $10,000. The Prism Fund invests in commercial property, consumer, legal, art, and corporate asset classes. This fund comes with a management fee of 1.5%.

If you see yourself as a more sophisticated investor willing to take on more significant risks in pursuing higher returns, consider checking out Yieldstreet.

9. HappyNest

Best for Simplicity

With HappyNest, you can purchase a REIT that will invest your money into commercial real estate. You can get started in only a few minutes with just $10.

HappyNest is a unique platform because lets you use your everyday spending to invest in real estate. You only need to kink your debit or credit card to your HappyNest account. HappyNest will round up every purchase, turning your loose change into shares that earn dividends from real estate.

For example, if you purchase lunch for $8.25, the app will round up to $9 and deposit $0.75 into a pool. When this pool hits $5, HappyNest will automatically invest your money in purchasing more shares. This way, you automatically invest in real estate without changing your spending habits.

HappyNest doesn’t yet have a proven track record like other real estate investing apps on this list. But we included them because of how easy it is to get started. I understand how intimidating it could be to get into real estate investing, and HappyNest is a great place to start.

With the advent of real estate investing apps, gone are the days when you have to worry about receiving a call from a tenant in the middle of the night or endless paperwork.

Begin Your Real Estate Investment Journey Today

The apps covered in this article are just some of the many ways you can invest in real estate. The main advantage of investing through an app like Roofstock or Fundrise is the low barrier to entry compared to purchasing a physical property. And gone are the days when you have to worry about receiving a call from a tenant in the middle of the night or endless paperwork.

Instead, you can begin your investing journey with $10 while sitting on the couch. Before you sign up, however, take a close look at each real estate app to ensure you invest in the right one. You can do that by reading our individual reviews and checking reviews from other experts and existing users.

If you have $15,000 stashed away, you’ll want to put that money to work. If you don’t, inflation can quickly eat away at your nest egg. Plus, the current rise in interest rates has made it worthwhile to have some money in savings accounts again.

But where should you invest your $15,000? That depends on when you’ll need the money, whether you want it to grow for a few years, a few decades, or longer. In the meantime, you’ll want to consider how much risk you’re willing to take to get a reasonable return.

16 Ways to Invest $15,000 in 2023

To help you figure out how to invest $15k, I compiled a list of 16 of the best options. Keep reading to find out where I think $15,000 should be invested in early 2023 and how you can get started today.

1. High-Yield Savings Accounts

If you have $15,000 to invest but plan to use the cash in the next few years, a high-yield savings account could be the way to go. The best high-yield savings accounts are FDIC-insured, so you are protected up to $250,000 per depositor per account. Plus, saving account yields are much higher than in the last few years, particularly when looking at the top online banks.

Take the high-yield savings account from UFB Direct, for example. This account offers 3.83% APY on savings, with no minimum deposit requirements or hidden fees. It comes with a complimentary ATM card you can use to access cash when you need to, and you earn the same exceptional yield whether you put your entire $15,000 nest egg in this account or only part of it.

2. Auto-Pilot Investing

You can invest $15,000 over a period of time by automating your investment contributions. You can utilize this strategy with Acorns, a savings app which lets you “round up” all your purchases and invest the difference with no added work on your part.

Acorns will automatically invest your money into diversified portfolios of ETFs built and managed by professionals. The highly-rated Acorns app makes it easy to watch your money grow over time.

Interestingly, Acorns even makes it possible to invest your spare change and other money into a Bitcoin ETF. This means your investments can grow over time along with the value of Bitcoin, which seems to be the most relevant and long-lasting crypto investment available today.

Acorns also cost just $3 or $5 per month, depending on the features you want your account to have. You can learn more about Acorns and how it works in my Acorns app review.

3. Invest in Fractional Shares

Investing in fractional shares is another smart move, particularly if you have $15,000 tucked away but want to buy stocks. After all, fractional shares essentially let you buy pieces of popular stock without buying an entire share if you don’t want to. Your slice of each stock will grow commensurate with the stock’s value, just as if you owned a full share or several shares.

M1 Finance is one of the best platforms for investing in fractional shares, mostly because it lets you invest using its intuitive app, and investing transactions are commission-free.

With M1 Finance, you invest in “pies” that are made up of different stocks and ETFs, including fractional shares. You also get the chance to build your own pie or choose from expert pies crafted by experts with different goals in mind.

My M1 Finance review explains more about this investing app and how it works, so read it before you start.

The best part about real estate crowdfunding is that you don’t have to deal with renters or the grunt work of being a landlord.

4. Real Estate Crowdfunding

Another smart way to grow $15,000 involves investing in real estate without being a landlord. This option makes sense since it would be difficult to buy a physical property with just $15,000 to put down, especially considering closing costs and other fees.

My favorite real estate crowdfunding platform is Fundrise, and this account is perfect for investing anywhere from $10 to $15,000. Essentially, you can invest in an eREIT (real estate investment trust) with commercial and residential real estate holdings. Your account not only makes money off the rental returns on Fundrise properties, but the value of your shares can grow as the company sells properties, too.

The best part about real estate crowdfunding is that you don’t have to deal with renters or the grunt work of being a landlord. You just invest your money and wait for a solid return (although returns are never guaranteed.)

That said, Fundrise has done well so far. Investors in the platform earned an average yield of 22.99% in 2021, and those invested in 2022 earned an average yield of 5.40% as of the third quarter of 2022. You can read more about this company and how it works in my Fundrise review.

In the meantime, you can also check out another real estate crowdfunding platform called Realty Mogul, which works similarly. The main difference between Fundrise and Realty Mogul is that Realty Mogul requires you to be an accredited investor, whereas Fundrise does not in most cases.

5. Open a Brokerage Account

Next up, you can always consider opening a brokerage account with your $15,000. You can do this with nearly any online brokerage platform, from major players like Vanguard and Fidelity to investing apps like M1 Finance and Robinhood.

Opening a brokerage account lets you invest for the future outside of a retirement account, allowing you to access your money by selling shares at any time without waiting until age 59 ½.

You can use your brokerage account to invest in index funds that track an index like the S&P 500, or you could get started investing in dividend stocks. You can also use a brokerage fund to buy individual stocks, bonds, ETFs, etc. The choice is up to you.

Maybe you want to invest in the stock market but are unsure how to get started or where to place your investments. In that case, hiring a robo-advisor could be your best move.

Robo-advisors use computer algorithms and statistics to determine the best ways to invest money, eliminating the need for a human advisor. Robo-advisors also tend to cost less than regular advisors, meaning you get to keep more of your gains over time.

Betterment is the robo-advisor I normally recommend for several reasons. Betterment makes it easy to invest automatically, and they ask you questions to assess your risk tolerance and get a better handle on your goals.

My Betterment investing review explains how the platform works. One standout feature is the price – Betterment fees start at just 0.25% on investment accounts. This compares very favorably to the 1% or more that most financial advisors charge.

7. Open a Roth IRA

If you’re looking for a way to save part of your $15,000 for retirement, consider opening a Roth IRA. This type of retirement account is only available to individuals whose incomes fall under certain thresholds, yet it lets you save money for retirement on an after-tax basis. In other words, you benefit from tax-free growth and tax-free distributions once you reach retirement age.

Another Roth IRA secret is that you can withdraw your contributions (but not earnings) anytime without penalty. This means you can take out the money you put into your account before age 59 ½ without paying income taxes on your withdrawals.

You can open a Roth IRA through platforms like M1 Finance and Robinhood or a robo-advisor like Betterment or Wealthfront.

8. Invest in Crypto

Investing in crypto may seem risky, given how things have been going over the last year. For example, a recent report from CNBC revealed that crypto values peaked in November 2021, and investors have lost $2 trillion in crypto-related wealth since that massive run-up.

Some cryptocurrencies like Bitcoin and Ethereum seem to have hit their bottom. At the very least, they may be getting close, and some currencies are bound to survive the crypto sell-off and stand the test of time.

If you want to invest part of your $15,000 in crypto to see where it goes, you can use an array of platforms to get started. Options include crypto investment platforms like Coinbase and investing apps like Robinhood and M1 Finance.

If you have high-interest debt and you also have $15,000, using your nest egg to pay off your debt can be an incredibly smart move. This is especially true since credit card interest rates have surged, and the average rate is now over 19%.

Paying off debt may not feel as satisfying as investing, but it should. After all, when you pay down high-interest debt, you’re essentially getting a “return” that lines up with the interest rate you’re paying.

For example, paying off $15,000 in credit card debt at 19% APR is like getting a 19% return on your money. Plus, paying off debt frees up cash flow you can invest over time.

10. Invest in Art and Collectibles

Did you know? You can invest $15,000 in famous works of art or even digital art. For example, you can invest in non-fungible tokens (NFTs), digital works of art that can grow in value over time.

I also like Masterworks, a crowdfunding platform for major works of art. Masterworks lets you invest in fractional shares of famous pieces of art that can be worth millions of dollars, and you make money as the art increases in value and is ultimately sold at a higher price.

Check out my Masterworks review to learn more about this company and how you can get started.

11. Certificates of Deposit (CDs)

Certificates of deposit (CDs) are a low-risk way to grow $15,000. This type of investment is similar to a high-yield savings account because your money is FDIC-insured in amounts up to $250,000 per deposit, per account. The difference is that you actually “lock in” your savings in a certificate of deposit (CD) for a set time.

SaveBetter is a great platform for CDs because they offer competitive yields and plenty of terms to choose from. The SaveBetter website is just a savings account and CD comparison platform, so you can use it to shop across many different banks in one place.

At the moment, SaveBetter offers fixed-term CDs with yields over 5%, and they even offer no-penalty CDs that let you access your money when you need it penalty-free.

12. Series I Savings Bonds

Next up, consider stashing part of your $15,000 into Series I Savings bonds. These bonds are government-backed, so your savings are guaranteed to grow at an agreed-upon rate. However, individuals can only invest up to $10,000 in electronic I bonds annually. Plus, you cannot access the money for at least 12 months, and you’ll pay a penalty of three months of interest if you cash in your Series I Savings bond within five years.

All this being said, Series I Savings bonds have some solid returns. The current rate is set at 6.89%, and it lasts through April 30, 2023. After that, the rate readjusts based on market conditions every six months.

13. Start a Business

A nest egg of $15,000 might also be enough to start a business, although you’ll want to be careful with the money and make sure you’re investing in something that can work for the long term. For example, you may be able to buy equipment you can use to start a service business. Of course, there are plenty of other home-based business ideas you could start with that much money in industries like catering, landscape design, tax preparation, herb farming, and more.

If you’re unsure about starting a small business, you can invest in other people’s small businesses with a platform called Mainvest. This platform lets you invest in regular, everyday businesses with a starting balance as low as $100 and targets returns between 10% and 25%.

Mainvest lets you get started with no investor fees, so it’s affordable.

14. Invest in Digital Real Estate

Next up is digital real estate. You can invest in websites like the one you’re reading right now. You can take steps to start your own blog or ecommerce business, or buy existing an existing website using a platform called Flippa.com.

Other types of digital real estate you can invest in include:

Affiliate websites built to earn passive income

Assets and land sold in the metaverse

Authority websites in a specific niche

Digital products like courses and printables

Email lists you can sell to others

Mobile apps

Paid membership groups

YouTube channels

Social media channels

Personally, I can say that my digital real estate investments have paid off significantly. I started Good Financial Cents more than a decade ago, and it has earned millions of dollars since those early days. From there, I added a YouTube channel that is also monetized, and I have sold a range of courses that have brought in big profits over the last decade.

If you’re wondering what it takes to get started as a blogger, you should check out my Make 1k Blogging course, which is free. True to the name, this course outlines exactly what you need to do to earn your first $1,000 online.

15. Invest in Farmland

Another way to invest $15,000 may sound unconventional, but it’s becoming increasingly popular. I’m talking about investing in farmland, but not going from town to town and buying up physical property.

With a platform called FarmTogether, anyone can invest in fractional shares of farmland that can earn real income over time. This platform aims for targeted net returns of 6% to 13% per year with a 2% to 9% targeted net cash yield. Not only does this platform make it easy to invest in farmland in a passive way that requires no work on your part, but it can also help you diversify your portfolio and include more types of investments outside of crypto, stocks, and bonds.

16. Open a Health Savings Account (HSA)

If you have a high-deductible health plan (HDHP), you can also invest in a Health Savings Account (HSA). An HSA lets you save for future healthcare expenses on a tax-advantaged basis, and contributions are tax-deductible in the year you contribute. In 2023, eligible individuals with an HDHP can contribute up to $3,850 to an HSA and families up to $7,750. People ages 50 and over with accounts can also contribute an additional $1,000 per year. This is what’s known as a “catch-up contribution.”

Note that only certain types of high-deductible health plans qualify for an HSA. Specifically, individuals need to have a minimum deductible of $1,500 in 2023, while families need a minimum deductible of $3,000. In the meantime, the total out-of-pocket amounts for health insurance plans are capped at $7,500 for individuals and $15,000 for families.

If you think you qualify and want to explore your HSA options, check out companies like HealthEquity and Lively. Both options let you invest your underlying HSA funds in the stock market, so your savings can grow over time.

As a side note, Lively HSAs are an especially good deal because they don’t have any regular account fees or hidden fees.

How to Invest 15k: Final Thoughts

The options outlined in this guide can work if you have $15,000 set aside and are ready to invest smartly. You could even spread your initial investment across several from the list to diversify your portfolio.

Whatever you do, make sure you read over the fine print of any new accounts you want to open and have a handle on the level of risk you’re willing to take on.

Also, never forget the golden rule of investing – that is, past results do not guarantee future returns. The investments on this list can help you grow $15,000 over time, but you can always lose money in the short term.

FAQ’s on Investing $15,000

Is $15,000 enough to start investing?

If you are starting from scratch, then $15,000 is a good amount to start investing. You can start by investing in stocks, mutual funds, ETF’s and crowdfunding real estate. However, it’s important to remember that investing involves risk, so it’s important to do your research before investing any money.

How can I invest $15,000 in 2023?

Assuming you have $15,000 to invest in 2023, the best way to invest the money would be in a diversified mix of stocks, bonds and real estate. This will give you the best chance of seeing a positive return on your investment while minimizing your risk. You can either invest in individual stocks and bonds yourself, or you can use an online broker to do it for you. You can also choose a robo-advisor that will charge little to no fees.

If you choose to go the DIY route, there are a number of online resources (including Investopedia) that can help you get started. If you prefer to let a professional handle it (like Edward Jones, Merrill Lynch, etc) most brokerage firms will offer a variety of investment options, including stocks, bonds, and even mutual funds.

Auditor general finds Real Estate Council of Ontario not fulfilling its mandate to protect consumers’ interests

Auditor general finds Real Estate Council of Ontario is not fulfilling its mandate to protect consumers’ interests. Photo by Peter J. Thompson/National Post

Reviews and recommendations are unbiased and products are independently selected. Postmedia may earn an affiliate commission from purchases made through links on this page.

Article content

With hundreds of billions of dollars invested in housing transactions, consumers and others should expect effective and robust regulation of the real estate sector, but a recent Auditor General of Ontario (AGO) report concluded quite the opposite.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

Article content

The AGO report said the Real Estate Council of Ontario (RECO), the agency responsible for regulating the provincial industry, is not fulfilling its mandate to protect the consumers’ interests. “The activities RECO performs … are not always effective and timely,” it concluded.

Financial Post Top Stories

Sign up to receive the daily top stories from the Financial Post, a division of Postmedia Network Inc.

By clicking on the sign up button you consent to receive the above newsletter from Postmedia Network Inc. You may unsubscribe any time by clicking on the unsubscribe link at the bottom of our emails. Postmedia Network Inc. | 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Financial Post Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

RECO was established in 1997 to promote a “fair, safe, and informed real estate market for consumers in Ontario through effective, innovative regulation of those who trade in real estate.” More than 78,000 salespersons and 20,038 brokers ply their trade with the 3,876 brokerages in Ontario, numbers that should make regulating them all a top priority for RECO.

RECO’s duties are supposed to include regular inspections of brokerages and thorough investigations of complaints against salespersons and brokers, but the AGO found severe gaps in the performance of both those duties. For example, RECO did not conduct an on-site inspection of 62 per cent of the brokerages in the five-year period from 2017 to 2021. Some brokerages have never been inspected.

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

The AGO’s audit of RECO’s data also showed that 88 per cent of the 2,643 complaints of alleged violations during the same period were summarily closed without a follow-up or an escalation to the investigation department. Similarly, RECO did not conduct a follow-up on 599 non-compliance notices sent to 491 brokerages issued for not remitting unclaimed consumer deposits to RECO.

RECO imposes fines for those found guilty of fraudulent behaviour, but they appear to be an insufficient deterrent. The average fine was $8,273, which is significantly less than the average commission earned on a residential transaction in large cities. It is estimated that 67 per cent of the violators that were fined were not required to take any remedial measures, such as further training or education.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

The primary reason for the mismatch between penalties and commissions is that RECO cannot determine what salespersons earn from any fraudulent behaviour.

And what about RECO’s responsibilities to prevent criminals from entering the real estate brokerage business? Surprisingly, RECO does not refuse to register individuals with past criminal convictions.

Similarly, Humber College, the institution that administers mandatory training and courses for aspiring realtors, reported 356 cases of large-scale deliberate and organized academic misconduct during examinations conducted in 2021, but not much was done by RECO to investigate them.

The AGO report is thorough in most instances, except for its concerns about money laundering in the real estate industry. The report speculates money laundering might be taking place and recommends actions to curb it, but a better approach would be to investigate any incidences of money laundering rather than speculating about it.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

As a regulator, RECO should also be proactive in protecting consumer rights, such as buyers being forced into blind bidding when multiple bids are placed for the same property. Many buyers end up paying tens of thousands of dollars, if not more, over the second-best offer, which has contributed to house-price inflation. Yet not much has been done by RECO to strike a balance between the rights of buyers and sellers.

RECO’s mandate is to regulate Ontario’s real estate sector, but it lacks the processes to deliver. For example, even though a 2014 regulation requires brokerages to keep all copies of written offers (bids) for a year, RECO does not collect data from brokerages to identify any fake bids, nor how much a homebuyer paid above the second-highest bid.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

As a regulator, RECO should collect all transaction-related data, including the contents of multiple bids, from brokerages for independent analysis to investigate accusations of irregularities and misconduct. If it did, RECO could share data-driven insights with the province to help improve legislation safeguarding the interests of buyers and sellers alike.

RECO falls under the purview of the Ministry of Public and Business Service Delivery, which should constitute a task force to oversee compliance of the dozens of recommendations AGO has made to address RECO’s shortcomings.

Real estate, especially housing, now constitutes a much larger share of the economy than in the past. Therefore, effective, independent and robust regulation of housing markets is a must to avoid a future great financial crisis, whose origins were in poor oversight of the housing sector in the United States.

Murtaza Haider is a professor of real estate management and director of the Urban Analytics Institute at Toronto Metropolitan University. Stephen Moranis is a real estate industry veteran. They can be reached at the Haider-Moranis Bulletin website,www.hmbulletin.com.

Share this article in your social network

Advertisement

This advertisement has not loaded yet, but your article continues below.

M1 Finance is a personal finance company that offers a variety of financial services, including investment management, portfolio analysis, and stock trading. The company is headquartered in Chicago, Illinois, and was founded in 2015.

If you read more about them in our M1 Finance review you’ll clearly see they are a top notch online broker that offers a wide array of investing and banking services and products to their clients.

But does that mean they are safe for you to invest your money?

We’re going to answer that question and whole lot more.

So, is M1 Finance secure?

The answer is yes. M1 Finance is a legitimate financial services company that is regulated by both FINRA and SIPC. Additionally, the company’s website states that it uses “industry-leading security protection” and is FDIC insured. Therefore, investors can rest assured that their money is safe with M1 Finance.

While M1 Finance is a safe and legitimate company, it’s important to remember that all investments come with risk. No investment is completely risk-free, so it’s important to do your own research before investing any money.

When did M1 Finance Start?

M1 Finance was founded in 2015 and is headquartered in Chicago, Illinois. They have grown quickly and now offer a variety of financial services, including investment management, portfolio analysis, and stock trading.

Currently, their AUM (assets under management) is over $6 billion with over 500,000 users (according to Wikipedia). While that’s certainly a large of assets for a relatively new firm, in comparison industry giant Fidelity currently has over $4.5 trillion in customer assets.

What Services does M1 Finance Offer?

M1 Finance offers a variety of financial services, including investment management, portfolio analysis, and stock trading. The company is FDIC insured and uses “industry-leading security protection.”

Investment Management: M1 Finance offers investment management services to help you grow your money. They offer a variety of features, including portfolio rebalancing, tax-loss harvesting, and automatic deposits.

Portfolio Analysis: M1 Finance’s portfolio analysis tools can help you understand your risk tolerance and invest accordingly. Their tools can also help you track your progress and see how your investments are performing.

Stock Trading: M1 Finance offers stock trading services so you can buy and sell stocks online. They offer a variety of features, including real-time quotes, charts, and analysis.

Is M1 Finance Free?

Yes, M1 Finance is free to use. There are no fees for opening an account, transferring money, or managing your portfolio. Additionally, there are no minimum balance requirements. You can start investing with as little or as much money as you want.

Hows does M1 Finance make money?

M1 Finance makes money by providing premium services to customers. These premium services include tax-loss harvesting and advanced analytics tools. They also make money through interest earned on cash balances in customer accounts, as well as from select securities transactions.

M1 Finance is a safe and legitimate financial services company that offers a variety of investment options, including individual stocks, ETFs, and mutual funds. The company has a strong history of providing quality services to its customers and has received numerous awards for its excellence.

What is SIPC?

The Securities Investor Protection Corporation (SIPC) is a nonprofit membership corporation that protects the customers of its members in the event of the failure of a member brokerage firm. It does this by providing funds to cover the missing securities and cash of customers up to certain limits.

Since its inception in over 50 years ago, the SIPC has helped recover over $141 billion in assets for over 770,000 investors. SIPC does not cover losses due to market fluctuations.

This means if you opened an account with M1 Finance and the company went bankrupt, SIPC would step in to help return your money. However, if you lost money due to bad stock picks, SIPC would not cover those losses.

What is FINRA?

The Financial Industry Regulatory Authority (FINRA) is a self-regulatory organization that oversees the brokers and firms that conduct business in the securities industry in the United States. FINRA is responsible for ensuring that firms comply with federal securities laws and regulations.

FINRA regulates M1 Finance to protect investors from fraudulent or abusive practices. The main functions they regulate include:

Licensing

Discipline

Marketing

Trading practices

Sales practices

FINRA also runs the Central Registration Depository (CRD), which is a database of information on brokers and firms.

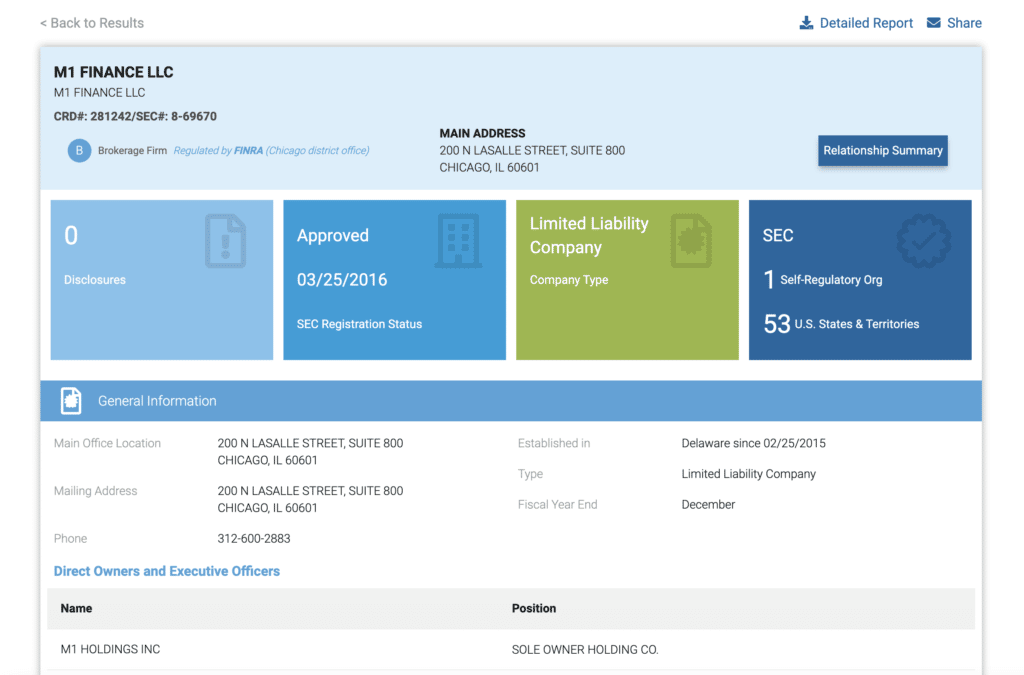

You can review M1 Finance’s information on Finra.org through their BrokerCheck database. Below is a screenshot of their FINRA listing:

A quick glance and you’ll find both their CRD#: 281242 and SEC#: 8-69670 since M1 Finance is also regulated by the SEC since they are currently registered in 53 states and U.S. territories.

You’ll see their LLC was approved in Delaware 02/25/2015 and their SEC registration status was approved 03/25/2016.

FDIC Coverage

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the US government that provides deposit insurance for banks and credit unions. FDIC coverage protects depositors up to $250,000 per account in the event of a bank failure.

There are times confusion of what FDIC covers and what they don’t. Below is a table that shows what type of investments FDIC is responsible for and what falls out of their jurisdiction.

DOES COVER

DOES NOT COVER

Checking accounts

Stocks

Negotiable Order of Withdrawal (NOW) accounts

Bonds

Savings accounts

Mutual Funds

Money market deposit accounts

Exchanged Traded Funds

CDs

Life Insurance Policies

Cashier’s checks

Annuities

Money orders

Municipal Securities

U.S. Treasury Bills

How Does FDIC Coverage work?

Here’s an example of how FDIC would work in the event of a bank closure:

Case Study: I have $100,000 in a personal checking account and $200,000 in a business checking account both at the same bank. How does FDIC insurance protect me?

If the bank you have your accounts with is FDIC-insured, then your personal and business checking accounts would be covered up to $250,000 each, for a total of $500,000 in coverage. This means that if the bank were to fail, the FDIC would reimburse you up to $250,000 for your personal checking account and up to $250,000 for your business checking account, for a total of $500,000 in coverage.

It’s important to note that FDIC insurance covers depositors’ accounts up to at least $250,000 per depositor per insured bank, so you would need to make sure that the bank you have your accounts with is FDIC-insured in order to be eligible for FDIC insurance coverage.

Now that we understand how FDIC coverage works, let’s see how this affects M1 Finance investors.

Does M1 Finance Carry FDIC Coverage?

First, you must understand M1 Finance is NOT a bank. They currently use Lincoln Savings Bank for all their banking products (M1 Checking). Lincoln Savings Bank is a member of the FDIC so that means you’ll get the same FDIC insurance as you would with any other bank.

What Type of Security Protection Does M1 Finance Use?

M1 Finance uses a few different types of security protection. One type is SSL, which is a secure socket layer. This encrypts the data that is sent between your computer and M1’s servers. This ensures that your information is safe and secure.

Another type of security protection that M1 Finance uses is two-factor authentication (2FA). This requires you to input a unique code, in addition to your username and password, in order to log in to your account. This code is usually sent to your phone via text message or an app.

This helps to keep your account secure, as someone would need both your login information and your phone in order to access your account.

Bottom Line – Is M1 Finance Legitimate?

Yes, M1 Finance is a legitimate financial services company. You don’t get to over $6 billion in investable assets and 500,000 total customers running a shady operation.

Another item I look at to see if an investment company passes the “sniff test” is to see if they have any “Disclosures” posted against them. A reportable disclosure could be information about certain criminal, civil, or customer complaints involving any of M1 Finance brokers. This could also include certain types of employment termination disclosures and bankruptcy discharges.

At this time M1 Finance has no such disclosure to report which means they have a clean track record.

As always be sure to do your own research in choosing the best investment platform for your needs.

FAQ’s on M1 Finance

What Type of Security Protection Does M1 Finance Use?

The company’s website states that it uses “industry-leading security protection.” Their data is protected with a military-grade 4096-bit encryption. They also offer two-factor authentication (2FA) which provides even more security on your personal information.

Is M1 Finance a SIPC Member?

Yes, M1 Finance is a member of the Securities Investor Protection Corporation (SIPC).

What are the cons of using M1 Finance?

M1 Finance may not be the best option for investors who want to trade frequently. The company doesn’t offer a platform that allows traders to buy and sell individual stocks.

Let’s say you’ve currently got a good amount of cash to invest. With the global financial recession building, opportunities are piling up. However, things could get worse in this bear market given we’re only nine months in. How would you invest it?

2022 has so far been a terrible year for both stocks and bonds. Real estate has outperformed stocks by over 20%. But even real estate is starting to fade as mortgage rates surged higher.

Nowhere to hide in 2022

How I’d Invest $250,000 Cash Today

After buying I Bonds, I’ve been accumulating a larger-than-normal cash hoard this year. Usually, I’ll have between $50,000 – $100,000 in my main bank account. But so far, I’ve accumulated over $250,000, partially due to a $122,000 private real estate investment windfall earlier this year.

In addition to accumulating cash, I’ve also been dollar-cost averaging in the S&P 500 on the way down. I’ve also been dollar-cost averaging in Sunbelt real estate on the way up. But these purchases are usually only in $1,000 – $5,000 increments.

Now that my cash balance is larger than normal, this is my thought exercise on how to deploy it. If you have less than $250,000, that’s fine too. I share the percentages of where I will allocate my money.

Background Info To Understand Our Investment Process

I’m 45 and my wife is 42. Our kids our 5.5 and 3.

We consider ourselves moderately conservative investors since we haven’t had regular day job income since 2012 for me and 2015 for my wife. We fear having to go back to work, not because of work itself but because we fear losing our freedom with young children. As a result, we are unwilling to take too much investment risk.

Although we don’t have day jobs, we do generate enough passive investment income to cover our living expenses. This is our definition of financial independence.

We also generate online income, which we usually reinvest to generate more passive income. Therefore, our cash pile will continue to build if we don’t spend or invest the money.

For life goals, we both want to remain unemployed at least until our youngest is eligible for kindergarten full-time in 2025. This way, we can spend more time with both children.

After 2025, we might find day jobs or I might focus on becoming a professional writer. I enjoy being an author but it pays poorly.

We’re also looking to upgrade our home in one-to-three years. That said, my wife and children would be happy living in our current home for the next ten years. Buying another home is not a priority.

Our children’s educational expenses are on track after we superfunded two 529 plans. We also have life insurance and estate planning set up. Therefore, there’s no major big ticket items coming up.

Here’s how we’d invest $250,000 cash in today’s bear market. This is what we’re doing with our own cash and not investment advice for you. Please always do your own due diligence before making any investment. Your investment decisions are yours alone.

1) Treasury Bonds (60% Of Cash Holding)

Only about 5% of our net worth is in bonds, individual muni bonds we plan to hold until maturity. Our target annual net worth growth rate is between 5% to 10% a year, depending on economic conditions. As a result, being able to earn up to ~4.8% on a 1-3-year treasury bond is enticing.

At the same time, I’m always on the lookout for a nicer home because I believe living in a great house is the best way to enjoy our wealth. Think about all the time we spend at home nowadays.

There is no joy or utility derived from owning stocks, which is one of the reasons why I prefer investing in real estate over stocks. However, dividend stocks do provide 100% passive income.

Once the 10-year bond yield reached 4%, I decided to purchase the following Treasury bonds totaling $142,872.91.

$101,736.74,000 worth of 9-month treasury bills yielding 4.2%.

$10,766.89 worth of 1-year treasury bills yielding 4.3%

$15,501.33 worth of 3-year treasury bills yielding 4.45%

$14,867.95 worth of 2-year treasury bills yielding 4.38%

Although locking in a 4.2% to 4.45% return won’t make us rich, it will provide us peace of mind. We also already feel rich, so making more money won’t make us feel richer. Our focus is on optimizing our freedom and time.

Here’s a tutorial on how to buy Treasury bonds, which includes some buying strategies to consider. I will buy more Treasuries if the 10-year reaches 4% again, as you can purchase an unlimited amount, unlike I Bonds.

The one-year Treasury bonds yielding ~4.73% is especially attractive right now. The reason why is because it’s so much higher than the current 10-year Treasury bond yield at ~3.58%. As inflation and interest rates fade over the next 12 months, one-year Treasury bonds and longer durations will look more and more attractive.

The remaining 39.9% of our cash will be invested in risk assets.

2) Stocks (10% Of Cash Holdings)

Roughly 27% of our net worth is in stocks. It was about 30% at the beginning of the year. Thanks bear market!

The range has hovered between 20% – 30% since I left work in 2012. Since I started working in equities in 1999, I’ve done my best to diversify away from stocks and into hard assets.

My career and pay were already leveraged to the stock market. And I saw so many great fortunes made and lost during my time in the industry. When I left work, I continued my preference of investing mostly in real estate.

Unfortunately, we front-loaded our stock purchases in 2022 through our kids’ Roth IRAs, custodial accounts, SEP IRAs, and 529 plans. For over 23 years, we’ve always front-loaded our tax-advantaged accounts at the beginning of the year to get them out of the way.

Most of the time it works out, some of the time it doesn’t. That’s market timing for you. But we do get to front-load our tax-advantaged investments again in 2023, which will prove to be better timing if the S&P 500 stays depressed.

In addition to maxing out our tax-advantaged accounts, we’ve been regular contributors to our taxable online brokerage accounts. After all, in order to retire early, you need a much larger taxable investment portfolio to live off its income.

No Rush To Buy Stocks

If the Fed insists on raising the Fed Funds rate to 5% and ruin the world, then the S&P 500 could easily decline below 3,600. And if earnings start getting cut by 10%, then the S&P 500 could decline to 3,200 based on the median historical P/E multiple.

With investors able to get a guaranteed 4%+ return in Treasuries, it’s hard to see the S&P 500 rebounding strongly until the Fed admits inflation has peaked.

Given the situation, I’m just buying in $1,000 – $5,000 tranches after every 1% – 2% decline through the end of the year. If the S&P 500 goes below 3,600, I will increase my investment size to $3,000 – $5,000 a trade.

If I was in my 20s and 30s, I would allocate 60% of my cash to buying stocks instead. 30% would go to online real estate and the rest to Treasuries and education.

3) Venture Capital / Venture Debt (20% Of Cash Holding)

I enjoy investing in private funds because they are long-term investments with no day-to-day price updates. As a result, these investments cause little stress and are easy to forget about.

I’ve already made capital commitments to a couple venture capital funds from Kleiner Perkins. I also made a capital commitment to Structural Capital, a venture debt fund. As a result, I will just keep contributing to these funds whenever there are capital calls.

I expect venture debt to outperform venture capital (equity) during this time of higher rates. Venture debt is a lower risk way to generate returns in private companies.

The biggest downside to investing in these funds is higher fees. We’re talking 1-3% of assets and 20-30% of profits.

4) Real Estate (10% Of Cash Holding)

Real estate is my favorite asset class to build wealth. It provides shelter, generates income, and is less volatile. Unlike with some stocks, real estate values just don’t decline by massive amounts overnight due to some small earnings miss. Real estate accounts for about 50% of our net worth.

No matter what happens to the value of our current forever home we bought in 2020, I’m thankful it has been able to keep my family safe and loved during the pandemic. When it comes to buying a primary residence, it’s lifestyle first, investment returns a distant second.

All the memories, photos, videos, and milestones our kids have achieved in our current house are priceless. Even when I was suffering from real estate FOMO earlier in the year, our kids said they prefer our much cheaper home. As a real estate obsessed father, that meant a lot.

Their response showed me the price of a home isn’t necessarily the main thing that makes it nicer. The house layout and its familiarity matters a lot too.

Given my wife and kids are happy in our home, I shouldn’t try to buy another one so soon. Ideally, we live in our current home for at least five years (2025), save up a lot more money, and comfortably upgrade based on my net worth home buying rule.

Therefore, I will continue to dollar-cost average into private real estate funds like Fundrise that invest in single-family homes in the Sunbelt. Prices and rents are cooling. However, Sunbelt real estate should be a long-term beneficiary of demographic trends, technology, and work from home.

I will be investing in $1,000 – $3,000 tranches through the end of the year.

5) Debt Pay Down (0% Of Cash Holding)

In a high inflation and rising interest rate environment, I’m not paying down any extra mortgage debt. I already paid down some mortgage debt at the beginning of the year when inflation was high and Treasury bond yields were low.

At the time, it was a suboptimal move since it’s best to keep your negative real interest rate mortgage for as long as possible. High inflation was paying off the mortgage debt for me. But I paid off some mortgage debt anyway because it felt good and I was uncertain about stocks.

In retrospect, paying down some mortgage debt in 2021 was the right move as it saved me from losing ~20% had I invested the cash in the stock market. Hence, if you have debt, consider following my FS DAIR investing and debt pay down framework. This way, you’re always making financial progress.

Today, with inflation still high but Treasury bond yields much higher than mortgage rates, it makes no sense to pay down a negative interest mortgage rate. Instead, it’s better to buy Treasury bonds and live for free, which I’m doing.

If you have revolving credit card debt or auto loan debt, I’d follow my FS DAIR framework and accelerate paying down principal. You want to benefit from rising interest rates not get hurt by it.

Just make sure you don’t compromise your liquidity too much in a bear market. Always have at least six months of living expenses in cash.

6) Education (0.1% of Cash Holding)

Education is the best investment. The paradox of education is it is extremely important to help you achieve financial freedom, yet it is also inexpensive or free today.

For example, for only $20 after tax you can order my bestseller, Buy This, Not That and immediately gain a competitive advantage to building wealth. You’ll also learn how to make more optimal decisions on some of life’s biggest dilemmas.

You could also subscribe to my free weekly newsletter and my free blog posts to stay on top of timely financial topics. The more you immerse yourself in money topics, the more you will learn and take appropriate action to help boost your wealth.

You can also go to YouTube, Khan Academy, or MOOC and watch hundreds of hours of free educational videos. Or you can pay for online courses to get even deeper into a subject.

Ignorance is no longer an excuse given how accessible education is today. Please allocate some of your budget to continuing education. Over time, the combination of experience and education will dramatically improve your confidence, wealth, and peace of mind.

Deployment Speed During Depends On Your Certainty

When the investment return is certain, it’s easier to invest cash. When you’re certain you don’t need the money, it’s easier to invest for longer durations as well. But not all investments are created equal.

I have deployed 60% of my $250,000 in Treasury bonds because I wanted to earn a higher return immediately. In fact, I’m actively trying to figure out a way to optimize our business cash as well. The investment is risk-free, so I have no fear.

I will most certainly fulfill my venture capital and venture debt capital calls when they come due. Otherwise, I will be banned from ever investing with these fund managers again. These investments have risks, but I want to diversify further.

I’m happy to keep investing in Sunbelt real estate funds, like I have since 2016, because I’m confident in the long-term demographic trend of relocating to lower-cost areas of the country. However, I’m also confident real estate prices and rents will fade over the next year, hence why I’m slowly legging in.

Finally, I’m certain I don’t like stock market volatility. I’m also uncertain how far rich central bankers will go to crush the middle class. As a result, I’m just nibbling and will focus on valuations.

It is discomforting to see your cash pile dwindle as you invest during a bear market. However, investing during a bear market tends to work out well over the long run. Further, if you maintain your income streams, your cash pile will replenish every month.

We know the average bear market lasts about 15 months. Hence, there’s a decent chance we could get out of this rut some time in 2023. Taking advantage of higher guaranteed returns while legging into risk assets today sounds like the right thing to do.

Reader Questions And Action Items To Invest Cash

Readers, how would you invest$250,000 cash in today’s bear market? Even if you don’t have $250,000, where would you invest your money? What type of investments do you think will generate over a 4.2% return over the next 12 months?

To gain an unfair competitive advantage in building wealth, read Buy This, Not That. It was written exactly for volatile times like these.I utilize my 27+ years of investing and finance experience to help you make better decisions.Click the image to pick up a copy today.

For more nuanced personal finance content, join 55,000+ others and sign up for the free Financial Samurai newsletter. I recap the week’s main events and share my candid thoughts.

One thing that made the pandemic especially hard was constantly feeling the anxiety of death. It’s one thing to worry about your own health and safety. It’s another thing to also have to worry about the health and safety of your little ones and elderly parents.

This winter has been especially difficult for little children due to the tridemic: flu, RSV, and COVID. My entire family has been sick off and on for two months. If I could donate my health points to my 5-year-old and 2-year-old so they could feel better, I would.

Alas, all my wife and I can do is protect them as much as possible. We feel like we’re always making risk-reward health calculations such as whether to go somewhere public or send them to school. At least we are lucky enough to be able to keep them home when they aren’t feeling 100%.

I got my parents to successfully visit us during Thanksgiving. However, with all the viruses going around, we’ve also had to throttle the time spent with them. I pray they don’t get sick as well.

How COVID Affects Life Insurance Rates

I like to quantify our feelings with data. Reconciling the two is a good way to understand whether what are are feeling is logical or not.

Luckily, I stumbled across an insightful article by Kate Dore from CNBC which discusses how COVID has changed the life insurance marketplace. It highlights the change in life insurance demand during the pandemic.

The gist of the article is that life insurers won’t know the full impact of COVID on mortality rates for perhaps 10 years. There are “long COVID” and unknown long-term effects of vaccines to study.

But if I were a betting man, which I am, I expect life insurance carriers to raise premiums to account for higher COVID risk. Therefore, the optimal move is to lock in an affordable life insurance policy now BEFORE more data comes to light.

Feels Good To Lock In Affordable Life Insurance

In December 2021, I was able to finally get a new 20-year term life insurance policy without a medical exam. For three years prior, I had been trying to get something reasonable due to the birth of our second child in December 2019.

My 10-year term policy was expiring in January 2023 and the renewal premium would jump from $40/month to $750/month! But I couldn’t find anything affordable because I had visited an overzealous sleep center in 2017. The business was brand new and the owners encouraged me to do all sorts of tests that went on my health record.

I felt so much relief once I got my new policy through PolicyGenius. It isn’t the $1 million coverage I had, but $750,000 is good enough to feel peace of mind. Further, the policy is a more reasonable $110/month and can be canceled at any time without penalty.

Just look at the annual change in retirees collecting Social Security during the pandemic. There was over a 35% drop since the beginning of 2020 likely due to an increase in elderly deaths!

Life Insurance Demand During The Pandemic

Everybody intuitively knows why anxiety, depression, sadness, and frustration have increased since the pandemic began. Such feelings sometimes translate into hate for other people, especially for people who seem to be doing better.

Hence, for your safety and happiness, it is important to make yourself look poorer and less successful than you really are during difficult times. Unless you’re trying to build a business, try not to stand out.

Below is a great chart that shows the historical interest in life insurance demand. We can finally quantify the anxiety many of us have been feeling since 2020.

Life insurance application activity was up 3.4% in 2021 after a record-breaking 3.9% in 2020, according to the MIB Life Index’s 2021 annual report. 3.4% and 3.9% doesn’t sound like huge increases, but it is for the life insurance industry.

I suspect once the 2022 data comes out, demand for life insurance will also be up again.

What’s more interesting is the 15.4% and 11% increase in what life insurers paid out in 2020 and 2021 according to data from the American Council of Life Insurers.

What Are Life Insurance Companies Going To Do?

The difference between the payout percentage and the application percentage is an indication of increased deaths and lower life insurance profitability.

A double-digit yearly increase in death benefit payouts is massive. Just think if you were running a business where your costs were up 11% – 15.4% YoY, but your revenue was only up between 3.4% – 3.9% during the same period.

You hope your expenses will normalize as mortality rates revert back to the mean (people go back to living longer). However, you’re not sure exactly when or if this will occur. At the same time, you also fear the long-term repercussions of COVID, which could lead to higher mortality rates (earlier deaths) and fewer premiums paid.

What does a life insurance company do in the medium-to-long run? It will likely raise premiums to make up for lower profitability. And one way to justify raising premiums is by implementing COVID-related questions in the future.

Life Expectancy At Birth, By Sex In The United States

Take a look at this CDC chart on the life expectancy at birth by sex in America. This is the first time in 21 years at least that life expectancy has declined.

Not only has life expectancy declined in America, it has declined by a lot. I would have expected maybe a 0.1-0.3-year decline in life expectancy. But not a 2-3-year decline in life expectancy!

Hopefully, life expectancy rebounds and reverts back to trend over time. But again, we don’t know for sure, which is why it’s best to lock in an affordable term life insurance policy before premiums go higher.

Much Less Anxiety Now

As soon as I locked in my 20-year term life insurance policy in December 2021, my anxiety about dying went away. I beat the clock, which was set to expire on January 3, 2023. My wife had already successfully doubled her coverage amount to match mine for less in 2020. The pandemic spurred us into action.

Now that I know there was an 11% – 15.4% YoY increase in death benefits paid out in 2020 and 2021, I feel even better about both of our new life insurance policies. My premium doesn’t just go toward paying a death benefit, it also goes towards improving my mental health.

If you were or are still feeling anxious about death during the pandemic, know you are not alone. The data backs up what you’ve been feeling all along.

Good thing there’s something we can do about it!

Reader Questions And Recommendations

Readers, what do you think about the life insurance application and payout data during the pandemic? Do the differences in percentages surprise you? Besides getting life insurance, how are you managing any anxiety you have around death and living the best life possible?

To search for affordable life insurance quotes, take a look at PolicyGenius. You’ll get real quotes in just minutes based on the information you submit. From there, you can smartly compare and go with the carrier that best suits your needs.

For more nuanced personal finance content, join 55,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Below are the newest 2023 Wall Street S&P 500 forecasts. The S&P 500 price targets range from 3,675 to 4,500. This implies returns of between -7.5% and +13% from the Dec 8, 2022 close of 3,963.

The key risks to the S&P 500’s performance include earnings cuts and valuation compression. If these two things were to happen, the S&P 500 could easily decline by 10% or more from current levels.

The S&P 500 could also see greater-than-expected earnings cuts and a valuation increase. This would occur if the market looks beyond the earnings cuts and expects better times ahead. The Fed could also pivot sooner-than-expected, thereby reigniting the bull market.

Personally, I believe the worst of the bear market was over when the S&P 500 hit 3,577 in October 2022. What matters most is what the Fed plans to do with interest rates. Come 1Q 2023, I think the Fed will have to pause its hikes and start cutting by the end of 2023.

As Asana billionaire CEO Dustin Moskowitz wisely quipped, “I’m CEO of the Asana company, but lately, Jay Powell has been CEO of the stock price.” Sadly, this scenario will likely continue to be true for the next 12 months.

A Recession In 2023 Is Almost A Certainty

With the yield curve the most inverted since 1981, the U.S. economy will most likely go back into a recession in 2023 (90% chance IMO). Take a look at the chart below. It shows how a recession has always followed an inverted yield curve since 1970.

The inversion is causing me to invest 60%+ of my cash and cash flow into one-year Treasuries yielding 4.7%+. A 4.7% guaranteed return on the S&P 500 would bring the index to 4,150, excluding dividends.

4,150 is on the upper third of the various 2023 Wall Street S&P 500 price targets (3,675 – 4,500). Therefore, it makes sense for me to invest the majority of my funds earmarked toward stocks and bonds into one-year Treasury bonds. When investing, please learn to think in percentages.

Again, I’m a middle-aged man with two kids, a mortgage, a stay-at-home spouse, and no job. I can’t afford to take too much risk. Otherwise, I’d end up employed!

2023 Wall Street Forecasts Of The S&P 500

Shoutout to Sam Ro from Tker.co for putting these estimates and summaries together in his newsletter. Here are 16 Wall Street S&P 500 forecasts for 2023 segmented by Bearish, Neutral, Positive, and Bullish.

Don’t forget to participate in the one-question survey below on where you think the S&P 500 will go in 2023. Let’s see if you got what it takes to be a good Wall Street strategist!

Bearish 2023 S&P 500 Forecasts

Barclays: 3,675, $210 EPS (as of Nov. 21, 2022) “We acknowledge some upside risks to our scenario analysis given post-peak inflation, strong consumer balance sheets and a resilient labor market. However, current multiples are baking in a sharp moderation in inflation and ultimately a soft landing, which we continue to believe is a low probability event.“

Societe Generale: 3,800 (as of Nov. 30) “Bearish but not as bearish as 2022 as the returns profile should be much better in 2023 as Fed hiking nears an end for this cycle. Our ‘hard soft-landing’ scenario sees EPS growth rebounding to 0% in 2023. We expect the index to trade in a wide range as we see negative profit growth in 1H23, a Fed pivot in June 2023, China re-opening in 3Q23 and a US recession in 1Q24.”

Capital Economics: 3,800 (as of Oct. 28) “We expect global economic growth to disappoint and the world to slip into a recession, resulting in more pain for global equities and corporate bonds. But we don’t anticipate a particularly prolonged downturn from here: by mid-2023 or so the worst may be behind us and risky assets could, in our view, start to rally again on a more sustained basis.“ I’ve personally never heard of these guys before.

Morgan Stanley: 3,900, $195 EPS (as of Nov. 14) “This leaves us 16% below consensus on ’23 EPS in our base case and down 11% from a year-over-year growth standpoint. After what’s left of this current tactical rally, we see the S&P 500 discounting the ’23 earnings risk sometime in Q123 via a ~3,000-3,300 price trough. We think this occurs in advance of the eventual trough in EPS, which is typical for earnings recessions.“