While some payments companies, including Stripe, Brex, Fidelity National Information Services and Klarna, have grabbed headlines with big job cuts, other payments players, including Wise, VizyPay and Papaya Global, are pressing ahead with big plans for hiring in 2023, despite the threatening economic forecasts.

The cross-border payments company Wise plans to add 250 U.S. employees in an approximately 40% boost to its headcount as it builds out its operations in North America from its headquarters in London.

Wise currently has about 600 employees in the U.S. spread across three offices in Austin, Tampa and New York City, Wise Chief Technology Officer Harsh Sinha said in an interview last week. That U.S. workforce grew about 78% over the past year, up from about 340 at the end of last year, a spokesperson for the company said.

North America is Wise’s fastest-growing market, with revenue from the region jumping 58% for the first six months of its fiscal 2023 year, from April to October, to $105 million, compared to the same period the prior year. That’s a big reason for the company focusing on growth in the region, Sinha said.

“We see a lot more momentum growth coming from the U.S. so we continue to invest more,” he said in the interview.

The CTO notes that Wise, which launched its business as TransferWise in 2011, has been profitable on a net basis in each of the past five years. He said the downturn that’s leading other companies to cut back presents an opportunity for Wise to hire needed talent.

“While everybody else is trying to figure out other aspects of cutting costs, we continue to grow,” he said.

In particular, Wise is doubling down on hiring in Austin where it expects to have its broadest cross-section of roles, including in engineering, product development, customer service, operations and sales. The company expects its headcount in the city to double to 200 employees from about 100 currently.

Austin is increasingly a tech center in the U.S. with tech companies moving there and many across industries opening offices in the city as they add tech staff there.

Wise is building its tech ranks as it focuses on revving up international payment with an emphasis on “instant” payments, or those that take place in 20 seconds or less. Sinha asserted that about half of its payments move at that rate. Overall, the company moves about $11 billion in payments volume per month, he said.

That kind of speedy payment is revolutionary in a cross-border payments sphere that has for decades been characterized by slow, inefficient transactions.

Currently, Wise’s biggest office is in Tampa, where it has about 450 employees, and it will remain the biggest, with plans to hire about 90 workers next year, the spokesperson said. That office has people management roles as well as those in operations, and customer service.

The New York office has 50 employees and will add 15 in 2023. That outpost includes banking, compliance, engineering, business development and marketing roles.

Worldwide, Wise has about 4,300 employees across 18 offices, the spokesperson said. Given its international business, the company also tracks the nationalities of its employees and says they represent 110 nationalities.

The payments processing fintech VizyPay also has plans for significant hiring next year. The company, based in Waukee, Iowa, is targeting the addition of 120 employees next year for a more than doubling of the employee headcount, according to Ericka Rivera, a spokesperson for the company.

VizyPay is in the business of providing processing services to merchants, with a sweet spot in meeting demand from businesses in small towns and rural communities.

VizyPay, which also operates with hundreds of contractors, said in a press release earlier this month that it promoted two company veterans to lead a department that’s standardizing and streamlining its employee training and career development processes ahead of the hiring binge.

“As we look to continue growing and hiring in 2023, this new department will get the processes and support structure we need in place,” VizyPay CEO Austin Mac Nab said in the Dec. 13 release.

The company currently has 92 employees. It has already starting the “hiring blitz,” with a few recently added workers starting in January, said a spokesperson for the company.

The Federal Reserve and the Federal Deposit Insurance Corp. (FDIC) identified two deficiencies the 2021 resolution plan submitted by Credit Suisse and a shortcoming in the plan laid out by BNP Paribas, the regulators said Friday.

Credit Suisse has until May 31 to submit a revised living will that addresses governance weaknesses in the bank’s U.S. operations, the regulators said. The living will — a roadmap to resolve the bank quickly if it fails or falls into bankruptcy or distress — lacks detail and necessary information, indicating the bank may not have given the plan “appropriate internal review and coordination” before it was submitted, the Fed and FDIC said.

The regulators are giving the bank until July 2024 to show it has remediated weaknesses in cash flow forecasting. Credit Suisse last month warned of a $1.6 billion loss in the fourth quarter — hardly the first quarterly loss the bank has telegraphed this year as it recovers from the Greensill and Archegos scandals.

Credit Suisse clients withdrew $88.3 billion from the bank between Sept. 30 and Nov. 11 — during which time the bank announced a far-reaching retooling.

The Swiss bank is “committed to addressing the issues raised within the required time frame,” it said in a statement seen by Bloomberg.

“The bank has taken, and continues to take, significant steps to enhance its resilience, including investments in controls, processes and technology,” Credit Suisse said, according to Reuters.

Additionally, the Fed and FDIC are giving BNP Paribas until July 2024 to submit a living will that adequately describes how securities repurchase agreement activity — such as daily trading and settlement, oversight and risk management — would remain uninterrupted in the bank’s U.S. operations.

A shortcoming is less severe than a deficiency, but the regulators made clear, in a letter to the bank last week, that the weakness would become a deficiency in their eyes if it received no further attention. BNP Paribas’ 2021 living will did not incorporate feedback the regulators suggested on the bank’s 2018 resolution plan.

BNP Paribas declined to comment to Bloomberg and did not immediately comment to Reuters.

The foreign banks are not the only institutions the Fed and FDIC saw falling short in their living wills. The regulators last month gave Citi until Jan. 31 to submit a “mapping document” aimed at resolving weaknesses related to data quality and data management concerns previously identified in an October 2020 enforcement action.

Taxes are our largest ongoing liability. As a result, it behooves us to optimize our taxes as much as possible. This post will discuss all the smart money-saving tax moves to make by year-end.

After fake retiring in 2012, my desire to maximum my income went away. Instead, I wanted to shield as much income from taxes as legally possible. Paying six figures in taxes a year for more than a decade felt good enough.

After ~$200,000 per person and $250,000 per married couple, the Alternative Minimum Tax kicks in. Meanwhile, deductions start aggressively phasing out. Even in expensive San Francisco, there wasn’t any need to make more than $200,000 a year. So that was the upper income limit I targeted.

Income Target And Tax Optimization After Kids

Thanks to lifestyle inflation, economic inflation, and the need to now support a family of four, I’ve got a new household income target of up to $400,000.

$400,000 is certainly not a necessary household income to live well. It’s just the ideal income level where you earn enough to do what you want, but aren’t getting crushed by taxes. I’d like to pay an effective tax rate of no more than 30%.

A 25% – 30% effective tax rate is high enough to feel like you’re contributing to society. But it’s not so high where you’re feeling robbed by the government.

$400,000 is also the household income threshold where President Biden wants to raise income taxes. I’m pretty sure nobody wants to pay a 39.6% marginal income tax rate, especially if you’re really stressed at work.

For hardcore tax optimizers, the ideal household income is closer to a MAGI of $340,100 based on 2022 income tax rates. Up to $340,100, a married household’s marginal income tax rate is a reasonable 24%.

After about $200,000 per person or $400,000 for a family of up to four, I’ve noticed there is no incremental increase in happiness. Instead, making more money often creates more misery due to more work and more stress.

The majority of actions to reduce your taxes must take place during the calendar year. So if you want to pay less taxes, it’s time to get cracking.

Money-Saving Year-End Tax Moves To Make

Here are all the smart money-saving year-end tax moves to make.

1) Charitable Donations

Being able to give your time and money away to worthy causes is one of the best benefits of being financially independent. No longer will you always feel conflicted about whether you should save and invest your next dollar versus helping someone in need. You just tend to give more because you can.

Guidelines to claim deduction son charitable donations:

You’ll need to itemize deductions and file Form 1040.

The charity organization must be qualified with the IRS and be actively tax exempt. This excludes political candidates and organizations, as well as individuals.

Used items such as housewares and clothing must be in good condition or better for them to be deductible.

Donated vehicles can be deducted at fair market value if you meet certain requirements. For example, the charity must sell your car well below market price to a person in need, or the organization must make major repairs to increase the car’s value. Alternatively, you could qualify if the charity will use the car for purposes such as delivering meals to needy individuals.

If the total of your non-cash contributions is greater than $500, you’ll need to file Form 8283.

You’ll need a written record of all cash donations with the date, amount, and charity name.

And if you receive goods or services for a donation, you can’t deduct your entire contribution. The value of what you received must be less than your donation, and you can only deduct the difference.

If you are volunteering and performing services for a charity using your car, you can deduct mileage.

Travel expenses can be deducted if you go on a trip with a qualified charitable organization and you’re “on duty in a genuine and substantial sense throughout the trip” per the IRS.

Donations of property are generally deducted at fair market value based on what they would sell for on the open market.

You can avoid capital gains on appreciated stocks held over a year if you donate them to a charitable organization. The amount you can deduct is determined by the stock’s fair market value on the contribution date. Consider setting up a Donor Advised Fund for greater impact.

Giving Percentage Rates By Income

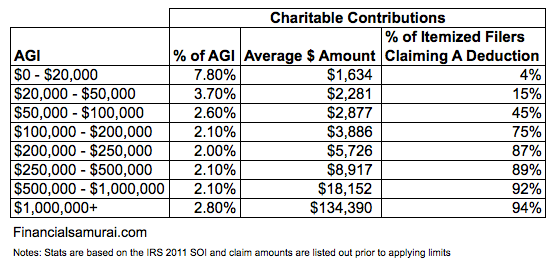

Here are some interesting statistics on average charitable contributions based on income for individuals claiming itemized deductions.

It is great to see the sub-$20,000 income group give away such a high percentage of their income. When I was working minimum wage service jobs, we tended to tip well to fellow minimum wagers. At lower income levels, it’s all about giving and helping each other survive.

Here’s another giving by income chart from the National Center For Charitable Statistics. It’s interesting to see the income groups that give the least earns between $200,000 – $1,000,000.

The reason is likely because this income group pays the most in taxes and earns the majority of income through W-2 income. After all, paying taxes is a form of charity since your tax dollars get redistributed to help others.

I’ve written a lot in the past about how households making $300,000, $400,000, and $500,000 a year in expensive cities are just living regular middle-class lifestyles. Part of the reason why is because a huge percentage of their income is going towards taxes.

Accelerate your charitable contributions to the current year if you want to lower your tax bill. One way to give is to strategically use your credit card when making a donation. Deductions are based on the date your card is charged, not the date you actually pay your credit card bill. In other words, you can make a donation via credit card on December 30, 2022 and not have to pay it off until January 2021.

2) Capitalize Losses On Bad Investments

If you own securities or property that have been declining and you’re below your cost basis, consider liquidating before year end if you don’t anticipate a recovery.

Losses on property held for personal use can’t be deducted. Only investment property losses can be written off. And you’ll also need to look at the net of your capital losses and gains. If your gains are higher than your losses, you’ll owe money on the difference.

Under the tax code, an individual may deduct up to $25,000 of real estate losses per year as long as your adjusted gross income is $100,000 or less and if you “actively participate” in managing the property. The deduction phases out as an individual’s income approaches $150,000. Individuals whose adjusted gross income exceeds $150,000 are not eligible for this deduction. This income threshold hasn’t changed for a while.

Note that you cannot deduct rental losses to your active income (e.g. day job income). Rental losses can only be deducted from passive income. You report your rental income and deductible expenses on IRS Schedule E. The IRS reports that roughly half of the filed Schedule E forms show losses.

Your big stock losses can offset any big gains in the calendar year. Any further losses can be carried over to the tune of $3,000 in capital loss deductions a year.

3) Increasing Expenses During Good Years

It’s good practice to anticipate and prepare for changes to your income in the upcoming year.

You should also increase your necessary expenses during a great income year. If you are having a bad income year, then defer such expenses until income improves. This is one of the best year-end tax moves to make for business owners.

If you are an employee, you can ask your employer to pay your year-end bonus in the following year if you want to defer income. Just make sure your employer will be around to pay you in the future.

4) Contribute To Tax Advantageous Retirement Accounts

You can make additional contributions to your 401k before year-end if you haven’t already maxed it out. The 2022 401(k) maximum contribution amount is $20,500. If you are a sole-proprietor, don’t forget to contribute the maximum to your solo-401(k).

In addition, you can make current year IRA and Roth IRA contributions until April 15 the following year. Or, you can wait to see what your modified AGI will be and then contribute accordingly.

For those of you who have experienced a particularly difficult year due to a job loss or other reasons, it may be beneficial for you to covert your traditional IRA into a Roth IRA. The Roth IRA conversion is a taxable event. However, the idea is to convert your traditional IRA when your marginal federal income tax rate is at its lowest point. Once taxes are paid on a Roth IRA, it grows tax-free and can be withdrawn tax-free.

In general, I’m not a fan of paying taxes up front with a Roth IRA, especially if you are in the 24% marginal income tax bracket or higher. If you are struggling financially, it may be even more difficult to bite the bullet and convert, despite being in a lower tax rate.

For high-income individuals looking for a workaround for the income limits on Roth IRA contributions, the backdoor Roth conversion is a solution. A nondeductible contribution can be made and then converted tax-free to a Roth IRA. This works because there are no income limits on non-deductible traditional IRA contributions or on Roth IRA conversions. However, be careful of the pro-rata rule.

The deadline to do a backdoor conversion for 2022 is Dec. 31. Congress seems highly motivated to eliminate the backdoor conversion in the future.

5) Deduct property tax

Property tax is an expense against rental income. Therefore, don’t forget to deduct it. Your primary mortgage property tax is also a deductible expense on your taxable income.

6) Business Tax Moves

[Graphic by: CKongSavage.com]

A business which is cash-based, not accrual-based, can defer taxable income to the following year by sending December invoices at the very end of the month. The reason this can work is the business won’t receive payment for those invoices until January or later, and the business’ taxable income isn’t captured until the date the cash comes in.

Companies and sole proprietors can also reduce taxable income in the current year by charging business related expenses in 4Q that they’d normally take in Q1 of the following year. If you expect your business to grow rapidly in the following year, then wait until the following year to load up on capital expenditure.

If you’re having a great business year, wait until the new year to cash your November and December checks in January. Although, there’s always a risk the vendor might disappear or go bust before you can cash your check. Make sure you know what the time limit is for cashing in a check as well.

Maximize Business Expense Deductions

One of the best year-end tax moves to make include maximizing your business deductions. If your business needs a vehicle and also is having a great year, consider buying a 6,000+ SUV or truck by 12/31. Let’s say you buy a $70,000 Range Rover Sport and use it 100 percent for business. Tax law allows you to deduct $70,000 (or a lesser amount if you would like – in this case, you use Section 179 expensing).

If the Gross Vehicle Weight is 6,000 pounds or less, your first-year write-off is limited to $10,000 ($18,000 with bonus depreciation as limited by the luxury auto limits). You can learn more about the tax rules for writing off a vehicle here.

Finally, a great private business strategy is to hire a close friend or relative who is in a lower tax bracket than your business tax bracket. Your friend or relative earns money while your business reduces its taxable income and receives services.

For example, you could hire your high school son for $6,000 to redesign your website. His $6,000 in earnings is tax-free given the standard deduction is much higher. Meanwhile, you reduce your taxable income by $5,000. Further, you hopefully get a slick new website while teaching your son about work.

The $6,000 earned by your son can then be invested in a Roth IRA. The income goes in tax-free, compounds tax-free, and gets to be withdrawn tax-free. As a result, opening up a Roth IRA for your children is a no-brainer! Both sides win.

Another great year-end tax moves to make is to make sure you don’t lose any money in your flex spending account. Check with your employer if your plan is eligible for a rollover of unused funds until March 15 of the following year.

If you’ve already run out of funds in your FSA but have things like medical work or fillings to do at the dentist, try to postpone them until next year if they aren’t urgent. That way you can save on taxes by allocating enough funds in next year’s FSA to cover those expenses.

If you’re planning on leaving Corporate America next year, get your physical done this year (usually free under preventative care). Also consider going to specialists to treat specific injuries. Maybe you need an MRI for a bum knee. Maybe you should finally see a pulmonologist for your asthma or COPD.

Try and get your money’s worth when it comes to healthcare. Don’t neglect physical ailments that are bothering you. They might get worse and more difficult to fix in the future.

8) Consider Revising Your Withholding

Even though you probably submitted your W-4 form to your employer ages ago, you can still file a revised form to make adjustments to the remaining pay periods left in the year. If you anticipate you haven’t withheld enough taxes so far this year, you can increase your withholding to help reduce penalties and fees when you file your taxes.

Check if you’ve already paid 100% of your current tax liability this year. If so and your AGI is less than ~$150,000, you should be able to avoid being charged a penalty. But you’ll need to have paid 110% of your current tax liability in the year to avoid getting dinged if your AGI is above ~$150,000.

This safe harbor method is generally the easier option to avoid paying a penalty. The alternative is to have withheld 90% of your tax liability, which can be difficult for freelancers and independent contracts to calculate.

If you are earning both W-2 wages and 1099 income, bumping up your January 15th estimated tax payment to compensate for having underpaid in previous quarters doesn’t work. Each quarter is treated separately with estimated taxes. However, withheld taxes on paychecks are treated as if they were paid throughout the whole year.

9) Review Your Retirement Contributions To Date

The maximum 401k contribution limit is $20,500 for 2022 and $22,500 for 2023. You should max out your 401(k) if you are in the 24% marginal federal income tax bracket or higher to save on taxes. Maxing out your 401(k) every year is one of the best year-end tax moves to make.

Even though this is the season of giving, don’t forget to pay yourself first. Take a look at how much you’ve contributed to your retirement accounts so far to date. Then make additional contributions to the maximum.

10) Set Up A Revocable Living Trust

If you haven’t talked to an estate planning lawyer yet, please do so. Setting up a revocable living trust is vital if you have dependents. Not only does a revocable living trust help protect your assets, it also helps with the orderly distribution of assets in case of your untimely demise. Finally, a revocable living trust is usually cheaper than going through probate court. The public has access to all your finances in probate.

While on the topic of estate planning, please put together a Death File as well. The Death File is like a hyper-detailed will that includes all your accounts, passwords, important people to contact, and your wishes. You should also include audio and video recordings in your Death File as well, so there is less ambiguity.

11) Maybe Finally Get Married

The marriage penalty tax has all but disappeared after the Tax Cuts and Jobs Act was passed in 2017. If you’ve been on the fence about marrying due to a higher tax bill, you really don’t have to worry any more.

It’s only married couples making over $500,000 who will likely pay more taxes together than as unmarried individuals. If one partner earns an income in the $200,000 – $400,000 range, while another partner earns income below $100,000, there will likely be tax benefits if the couple gets married.

12) Start A Business

Starting a business might be too late as a year-end tax move. However, there’s always next year!

You can either incorporate as an LLC or S-Corp or simply be a Sole Proprietor. As a sole proprietor, no incorporation is necessary. Just file a Schedule C and 1040.

For 2023, every business person can start a Self-Employed 401(k) where you can contribute up to $66,000 ($22,500 from you as an employee and ~20% of operating profits from the business). In other words, to contribute the maximum to a Solo 401(k), your business needs to make around $240,000 in operating profits.

Further, all your business-related expenses are tax deductible as well. If you want to go to Hawaii to see a prospective client, you can deduct your travel-related expenses. If your parents so happen to live in Hawaii, it’s like getting a discounted trip to see them.

The first step is to launch your own website to legitimize your business. The next step is to obviously go try and make some income! Most expenses related to the pursuit of such income should be considered a business expense. Below is an income statement example from a sole proprietor.

Start a simple business to pay less taxes and contribute more to pre-tax retirement accounts

Study Up On The Latest Tax Rules

We all need to spend several hours each year reviewing and understanding the latest tax rules. Given the tax code is tens of thousands of pages long, spending several hours a year learning them is the least we can do.

Every year, there are many new propositions and tax laws that pass that may affect your future tax liabilities.

For example, California recently abolished Proposition 58 in place of Proposition 19. The new proposition reassesses the value of a rental property to market rate when it is passed to a child. This way, California can charge higher property taxes. For a primary residence, the value is also reassessed to market rate with a $1 million buffer.

Pay Attention To The Latest Estate Tax Exemption Amounts

Perhaps the most interesting tax information we should pay attention to are changes in the estate tax exemption amounts. If you are fortunate enough to have a household net worth higher than the estate tax exemption amount, more intentional spending and giving is in order.

By 2025, the Tax Cut And Jobs Act will expire. Under Joe Biden, there’s a high chance the estate tax threshold may go back down. For 2023, the estate tax exemption amount is an impressive $12,920,000 per person and $25,840,000 per married couple.

Let’s say the estate tax threshold per person declines to just $5 million per person in 2026. You currently have a $10 million net worth, the ideal net worth amount for retirement. If you die in 2026 and your net worth stays flat, you will have $5 million in estate tax exposure, or an estimated $2 million tax bill!

Please make realistic net worth and mortality projections. Paying a death tax on wealth you’ve already paid taxes on is a true waste.

Hopefully this article has given you some good year-end tax moves to minimize your tax liability.

Pay Your Taxes With Pride

For those of you who are paying more in taxes than the median household makes a year (~$75,000 in 2022), feel proud that you are contributing to society. Paying taxes could even be considered a form of charity after a certain amount.

Taxes are used to pay for defense, healthcare, infrastructure, food and shelter assistance programs, public schools, and more. If these things are considered good, then paying taxes should also be considered good.

It’s understandable that some people want to raise taxes on others without having to pay more themselves. Most working Americans don’t pay income taxes. However, if you are one of them, change your mindset.

Hopefully these great year-end tax moves will help you save money!

Reader Questions And Recommendations

Readers, what other smart money-saving year-end tax moves do you recommend making before year-end? What are some new tax rules for 2023 we should be aware of?

Pick up a copy of Buy This, Not That, my an instant Wall Street Journal bestseller. The book helps you make more optimal investing decisions so you can live a better, more fulfilling life. BTNT is on sale on Amazon right now.

For more nuanced personal finance content, join 55,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

2023 housing price forecasts from various institutions range from -22% to + 5.4%. There is no consensus as to which way house prices will go. However, the bias is towards the downside.

There is also the issue of forecasting the national median home price and the price of your local housing market. While we care about the national median home price forecast, we care way more about our local housing market forecast.

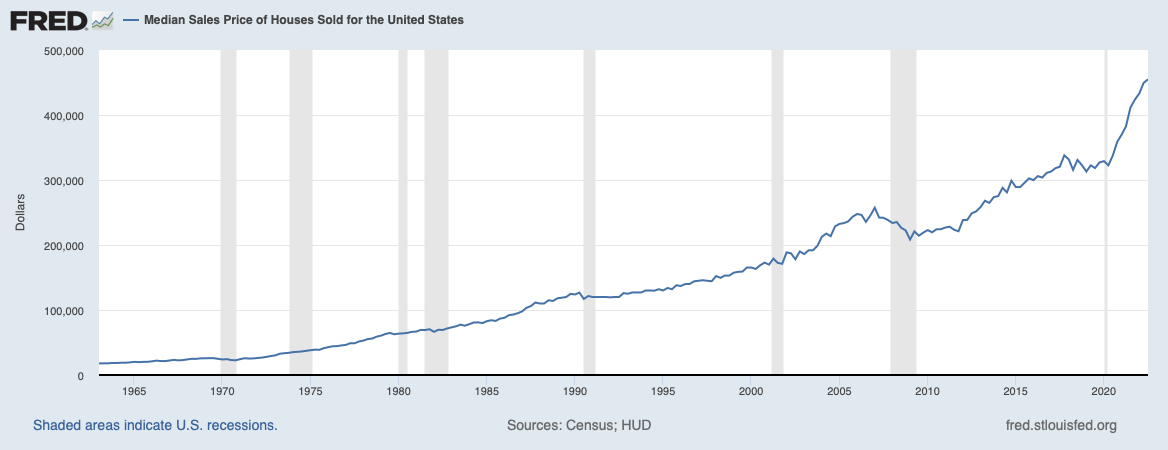

For background, I expected the median sales price in the United States to rise by 8% to 10% in 2022. My estimate was less bullish than the majority of firms expecting 15% – 18% price increases.

The 4Q2021 median home price was $423,600. The latest pricing data available, 3Q 2022, shows the median home price of $454,900, or a 7.4% increase. 4Q 2022 housing price data will be released in 1Q 2023.

2023 Housing Price Forecasts

Take a look at the housing price forecasts for 2023 from some popular real estate or real estate-related institutions. They are all over the place!

The Most Bearish Housing Forecasts For 2023

John Burns Real Estate Consulting (JBREC): -20% to -22%

Zonda: -10%

Goldman Sachs: -5% to -10%

Redfin: -4%

The Most Bullish Housing Price Forecasts For 2023

Realtor.com: +5.4%

CoreLogic: +4.1%

National Association Of Realtors: +1.2%

The Most Boring Housing Price Forecasts For 2023

Fannie Mae: -1.5%

Freddie Mac: -0.2%

MBA: +0.7%

Zillow: +0.8%

My Thoughts On The Extreme Housing Price Forecasts

When it comes to forecasting, it’s good to first look at the tail ends. It helps to see who is delusional and whether you have any blind spots.

Most Bearish Call

I like the work of John Burns Real Estate Consulting (JBREC). However, they are too pessimistic forecasting a -20% to -22% decline in housing prices in 2023. A 20% median home price decline would bring the national median home price down to about $364,000.

A 20% – 22% price decline would mean a GREATER decline than the one during the global financial crisis. Median home prices declined from $257,000 in 1Q 2007 to $208,400 in 1Q 2009, or -18.9%. Further, it took two years for national median home prices to decline by 18.9%.

It is improbable the national median home price will decline by more than it did during the global financial crisis in half the amount of time.

If we say this housing downturn is 30% as bad as the one from 2007 – 2009, then we’d get to a -5.7% housing price decline.

Most Bullish Call

On the flip side, there’s the +5.4% housing price forecast by Realtor dot com. Realtor dot com is a website that helps you find a realtor to buy or sell a home. The realtor pays a referral fee on closed transactions. The stronger the housing market, the more business Realtor dot com will generate.

It’s not a coincidence CoreLogic (+4.1%),the National Association Of Realtors (+1.2%), Mortgage Bankers Association (+0.7%), and Zillow (+0.8%) are all also looking for higher median house prices in 2023.

With a Fed-induced recession likely in 2023 and higher average mortgage rates, I think every forecast that shows an increase in 2023 housing prices is wrong.

My 2023 Housing Price Forecast

With an 75% conviction level, I expect the median housing price for 2023 to decline by 8% to $418,000. I’m assuming the median house price ends 2022 at $455,000.

The reasons include:

A global recession by the end of 2023

The Fed insisting on hiking to a 5% – 5.125% terminal rate even though inflation is clearly declining and annualizing under 2%

A higher risk-free rate makes investing in risk assets less appealing

An 8% decline in housing prices is disappointing for real estate owners. However, real estate has outperformed the S&P 500 by over 25% in 2022. Giving back 8% is not that bad, especially if you bought responsibility or have little-to-no mortgage left.

The reasons why I don’t expect home prices to decline by more than 8% are:

30-year fixed mortgage rates should decline by 2% – 3% from their peak of 7% by mid-2023. 4% – 5% 30-year fixed mortgage rates should bring back demand.

The Treasury bond market has stopped listening to the Fed. The 10-year bond yield did not move after the Fed raised rates another 50 bps on December 14, 2022. The huge yield inversion between the 10-year and the 3-month Treasury bond is saying the Fed is making a mistake. And retail mortgage rates are priced largely off the 10-year bond yield.

Consumers still have “excess” savings thanks to tremendous stimulus spending in 2020 and 2021.

There will continue to be an undersupply of homes. The vast majority of homeowners have 30-year fixed mortgage rates under 5%. Therefore, there’s no need for most to sell.

The will be a continued capital shift towards real assets and away from funny money assets like stocks, cryptocurrencies, and anything else that provides zero utility.

Downside Risks To My Negative Housing Price Forecast: Desperation

One of the biggest unknowns is how much new housing supply will come to market during the traditionally strong spring season. If there are too many desperate sellers, we could see home prices fall by more than 8% .

You also have funky scenarios where a house is priced too high and becomes “stale fish.” You might also encounter extremely motivated sellers going through a divorce. One short-sale can ruin the values of a dozen neighboring homes.

2023 inventory will likely still be at least 20% below 2015 – 2020 average

The other main downside risk to my negative housing price forecast is a more aggressive Fed. Although the Treasury bond market has stopped believing the Fed, a 5.125% Fed Funds rate will squeeze consumer debt borrowers. Everything from credit card rates to auto loan rates will go up.

A minority of thinly stretched borrowers can cause harm to the majority who have their finances in order.

Seeing prices fall by 8%+ in your local housing market is easy to see, especially if your housing market showed the most robust gains in 2020 and 2021. Prices in Boise and Austin could easily fall by 20% from their peaks before bottoming.

Biggest Upside Risk To My Negative Housing Price Forecast: Stealth Wealth

I may be underestimating the amount of liquid wealth potential buyers are holding. The amount of stealth wealth out there is more than we all know. Further, I may also be underestimating how much demand will return to the housing market if mortgage rates do decline by 2% – 3% in 2023.

Personally, I have a lot of cash and short-term Treasury bonds. So do all of my friends. I have a feeling, many Financial Samurai readers have an elevated amount of cash as well.

If many of us are going to be hunting for housing deals in 2023, will housing prices really decline by my forecasted 8%? Maybe not. I still believe house prices will decline, but perhaps by only 5% instead.

When it comes to housing prices, prices tend to get bid up quicker than they fall. Hence, buyers might only have a short window to take advantage of price discounts.

Mortgage Demand Highly Sensitive To Even High Rates

Take a look at this chart below. It shows a surge in mortgage purchase applications as the average 30-year fixed rate fell from 7.1% in October 2022 to 6.3%. 6.3% is still high compared to a year ago. But mortgage purchase applications went up 13.8%.

Hence, if mortgage rates fall to 4% – 5% by mid-2023, perhaps we will see a 25%+ increase in mortgage purchase applications. The longer the inactivity in real estate transactions, the greater the pent-up demand.

Even if all my properties decline by 10% on average in 2023, I don’t care because I don’t feel it. I will continue to raise my family in our primary residence. Then I’ll continue to collect my rental income to help pay for our lifestyles.

An asset that provides both income and utility is the best type of asset class to own. However, tenant headaches, maintenance issues, and property taxes can get to even the most patient real estate investors. As a result, a diversification of investments into stocks, real estate, bonds, and alternatives is recommended.

If you want to buy real estate in 2023, there will be plenty of opportunities to do so at more reasonable prices. The combination of declines in both housing prices and mortgage rates will make real estate more attractive by the middle of 2023.

When that time comes, I just hope nobody bids against me. Being able to buy my current forever home once lockdowns began on March 18, 2020 was ideal. If I had faced competition, I would have easily paid 4% more.

Loading …

Reader Questions And Suggestions

Readers, what are your housing price forecasts for 2023 and why? Are you planning on hunting for deals in 2023? What would cause you to sell your property in 2023?

If you want to invest in real estate more surgically, take a look at Fundrise. Fundrise primarily investments in single-family and multi-family homes in the Sunbelt. Its income fund is generating an 8%+ yield. Further, Fundrise is using its existing cash to hunt for distressed deals with 13-14% yields. I just spoke to Ben Miller, the CEO for an hour.

Pick up a copy of Buy This, Not That, my an instant Wall Street Journal bestseller. The book helps you make more optimal investing decisions so you can live a better, more fulfilling life.

For more nuanced personal finance content, join 55,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Minimalism and early retirement go together like peanut butter and jelly. Each item compliments the other. Minimalism helps get you to early retirement sooner because you are lowering your cost structure. Early retirement makes you want to simplify life so you can remain retired and enjoy your time more efficiently.

Since 2012, I’ve worked on becoming a minimalist with uneven results.

Ten years ago, I tried to sell my oversized house, but got no takers. It had two empty bedrooms we didn’t need. In 2017, we finally downsized. It felt much better to not have wasted space.

After giving away most of my dress clothes, my closet is pretty barren. But I still have a difficult time getting rid of old t-shirts that provide a lot of good memories.

Finally, I’ve maintained my one-car household for over 20 years. It’d be nice to go car free, but I’ve got two little kids to shuttle around.

For two years, I gave up on minimalism by buying a larger house in 2020. With the larger house came more furniture, more maintenance issues, and more cleaning time.

Now I’m intent on going back to minimalism and early retirement due to a series of unfortunate events. We have a tendency to collect more of everything. As a result, we naturally complicate our lives over time.

Become A Minimalist Because Everything Always Breaks

The more often things break, the more you need to spend time and money fixing them. Let me recap a list of things that have gone wrong that makes me want to get rid of things again.

After a nice five-day vacation in Lake Tahoe, I finished loading my car up with luggage and the children. With an energy drink in hand, I was finally ready to make the three-hour drive back to San Francisco. However, as I swung around to the driver’s side, I was startled by the site of a massive gash! WTF!

My car had been left overnight under the valet’s care and The Resort At Squaw Creek had failed to protect it. What transpired next caused me tremendous stress for the rest of the day as I had to 1) explain to my little ones why their trip home was being delayed; 2) spend a couple of hours in a car going to Reno to pick up a rental car; and 3) dealing with the insurance agency, The Resort, and the car rental agency.

In all, I wasted about nine hours of my life over 2.5 months due to this unfortunate situation. When it happened, I remember wishing I didn’t have a car. Dealing with accidents, flat tires, inevitable maintenance issues, towing, and tickets is not fun. Owning two cars would just double the trouble!

2) Random property issues

One of the reasons why I’m only investing in private real estate from now on is because something always breaks with one of my physical properties. Here are several recent examples:

A) In August, my tenant’s bike got stolen. Apparently, my sister and boyfriend left the side door unlocked, but there is no proof they didn’t lock the door. Nor is there proof they stole a $3,000+ bike I did not know was there. Ah, my love hate relationship with owning rentals.

B) In September, I got a notice at my rental from the Bureau of Street Use and Mapping Division. The notice said my planter boxes on my property were too high and had to be taken down. Huh?! The wooden planter boxes looked great and had been around for seven years. I had to spend $3,200 to remove them within two months.

C) In November, a different tenant discovered a cracked kitchen sink pipe on both sides that caused a leak. I had just remodeled the kitchen in 2020. How could the pipe crack so soon? Instead of relaxing on a Saturday, I had to trade text messages with my tenant to coordinate a handyman to take a look. Luckily, my handyman was available the next day and it only cost $150 to fix.

D) On a rainy Saturday in December, all my primary residence electrical outlets in my primary bedroom suddenly stopped working. I found an electrician who charged $145 an hour. After three hours of work, one hour for getting supplies at $85, and $50 in materials he solved the problem. I’m glad to have power again in my bedroom, but now I wonder what other random thing could go wrong.

3) Children getting non-stop colds

Before having children, I might get sick once a year for up to two weeks. Since my son started going to school in 2021, I’ve been getting sick twice a year for four to five weeks total. With my daughter starting preschool twice a week in 2022, she is also getting sick.

Given we’re both stay-at-home parents, my wife and I can’t help but catch their illnesses. For the past three months, at least two members of our household have always been sick.

There doesn’t seem to be any end in sight since parents will continue to send their kids to school sick because most parents need to work. They can’t afford to take too much time off to care for their sick children. I wonder if it’s a good idea to homeschool our kids during viral outbreaks and send them back once things calm down.

One of the reasons why my wife and I decided not to have more kids is because we don’t have the capacity to take care of more in the way that we want. An unhappy home full of fights and potential divorce would be counterproductive to raising kids.

In retrospect, having one kid was easy in comparison to having two. Having zero kids makes life even easier. But, of course, we wouldn’t trade our kids for the world. We just know our limits.

Being an early retiree without kids would probably force me to go back to work due to loneliness and boredom. There’s really only so much traveling and play one can do before both get boring.

4) A more and more complicated net worth

Money is awesome for being able to do more of what you want. The more money you have the more passive income you can generate. However, the more money you have, the more you can lose as well!

2022 is a great reminder of how quickly funny money can disappear in a bear market. At the extreme, people like Mark Zuckerberg have lost over $80 billion in the past twelve months.

Personally, I’ve lost a larger absolute dollar amount in 2022 than I did during the 2008 global financial crisis. Although my percentage net worth decline is not nearly as bad as the 35% decline I experienced in 2008, it still hurts.

The quick evaporation of stock market wealth is why I will likely always have a minority of my net worth invested in stocks. It’s hard to be disciplined to always sell stock gains to enjoy life.

Therefore, I’d rather invest my money in real estate and alternative assets. It’s nice to concurrently enjoy wealth and potentially make money at the same time.

However, the more different types of investments you have, the more complicated your net worth. The more complicated your net worth, the more you have to track. There are also more tax documents to file. Investing can be like filling a closet full of unnecessary clothes.

I enjoy running Financial Samurai. It brings me joy and purpose in fake retirement. However, every once in a while, some random tech issue pop ups.

For example, in December, my posts stopped releasing to various RSS feeds, like Feedly, every time they get published. My e-mail management system also stopped automatically picking up the posts. So I have to create each e-mail by scratch.

It’s not the end of the world since there are only about 2,000 RSS feed readers. My posts still get indexed by Google. Further, I can still manually send out my posts via e-mail that now take five minutes to create. It’s just annoying things just randomly stopped working.

Now I’ve got to spend up to $400 trouble shooting the issue. In the meantime, I’m recording more podcasts because they release to the RSS feeds. Publishing podcasts is a reasonable solution in the meantime. The show notes of each episode links to the posts.

If I just had Financial Samurai, or just had a podcast, or just had a weekly newsletter or just wrote personal finance books, early retirement life would be simpler. But these are the sacrifices I make to have an omni-channel presence. It’s been hard to prevent work creep over the years, which is why I limit my FS hours to 20 a week.

From 2009 – 2012 all I had was Financial Samurai. I had a minimalist online presence because I had a day job. Perhaps I should return to simpler times again.

A Simple, Minimalistic Life Is Wonderful

Staring at a blank canvas with black borders worth millions

The ironic thing about early retirement is that it frees up time to deal with these random problems that consistently occur in life.

Due to early retirement, I don’t need to hire a property manager to manage my rentals. Early retirement also enables us to take care of our little ones at home indefinitely if they are sick.

But even if you have tremendous free time, you still don’t want to deal with these issues. You’d much prefer to have fewer problems so you can do more of what you want. Since you rationally do the most enjoyable things with your free time, the opportunity cost for early retirees not doing things is greater.

For example, let’s say you have to skip work to take care of your kids. A bummer for sure. But at least you don’t have to work and will likely still get paid. As an early retiree, you might have to skip doing something fun for a week to take care of your kids.

Yes, this is a first-world problem. I’m just pointing out that everything is relative. With Lean FIRE, practicing minimalism helps free up even more valuable time.

Once you’ve got almost everything you want and experienced almost everything you’ve desired, it’s best to simplify.

Here are some things I will offload in the name of minimalism:

All clothes I did not buy or that don’t fit. I have too many oversized t-shirts that were given as free swag. I’ve also held onto some work clothes for 10 years just in case I return. But I’m never returning now.

Any shoes over two years old to protect my ankles from rolling over. The heels wear down, creating more risk.

Donate children’s books and toys to organizations that giveaway books and toys to needy families. During the pandemic, we accumulated a library of children’s books. I know other children between 1-5 will love them too. Giving the gift of education through books is the best.

If my condo tenant ever leaves, I will sell it if the conditions are fair. The condo is relatively low maintenance given there is an HOA and the condo isn’t big. When the time comes, I will happily reinvest the proceeds into a diversified private real estate fund.

Sell my primary residence if I ever upgrade our house again. No matter how much money you have, you can only live in one place at one time. No longer will I buy a new place and then rent my old place out since I’ve hit my physical property limit.

Reduce the average length of my posts by 20%. Shorter posts are easier to edit and easier to read. Further, it increases my chances of not burning out.

Becoming a complete minimalist may be a challenge given we still have two young children. However, we will try to instill in them the philosophy that “less is more.” Moderation is the key!

Reader Questions And Suggestions

Readers, have you embraced minimalism? What are some of the things you want more of and less of? Do you think minimalism and early retirement go hand-in-hand?

Check out Personal Capital, the best free tool to help you with tracking your finances and managing your investments. Also check out NewRetirement, an excellent tool specifically for helping you retire and stay retired.

Pick up a copy of Buy This, Not That, my an instant Wall Street Journal bestseller. The book helps you make more optimal investing decisions so you can live a better, more fulfilling life.

The first rule of financial independence is to not lose money. If you lose lots of money, you are ultimately losing valuable time. Losing time is the biggest financial mistake you can make because time is the most valuable asset.

Now let me introduce the second rule of financial independence: never expect your income to always go up. Expecting your income to always go up and to the right is the second biggest financial mistake you can ever make.

Life is not a straight line. Bad things happen all the time. If it’s not a pandemic that crushes your income, it might be a bear market. And if it’s not a bear market that leaves you jobless, it might be a health issue that prevents you from working.

The Biggest Financial Mistake Cost Me A Fortune

People over 40 don’t need to be told that life is both wonderful and difficult. For all of you still relatively early on your financial journey, please take heed.

Do not extrapolate the good times too far out into the future. If you do, you will likely make financial mistakes you will regret.

Back in 2007, at the time, I made the most amount of money in my career. I had gotten recently gotten promoted to Vice President and thought I had finally arrived! In my spreadsheet, I estimated I would “conservatively” make 10% more annually for the next five years. It seemed reasonable in a bull market.

When you’re flush with cash and have a promising career, why not reward yourself? So that’s what I did. I bought a two-bedroom, two-bathroom vacation condo in Lake Tahoe for $715,000. I thought it was a good deal because similar condos had sold a year earlier for $810,000.

Then in 2008, Bear Stearns and Lehman Brothers went bankrupt. The S&P 500 crashed by 38.5% and the housing market collapsed. Within a couple of years, my condo’s value plummeted to under $500,000. Neighbors were conducting short sales left and right, bringing everybody else down with them.

If only I had avoided the financial mistake of income extrapolation. I would be at least $300,000 richer today. Lesson learned.

Keep your income expectations conservative. If you do not, you may end up buying things beyond what you are capable of affording.

Feeling Like You Always Deserve More Income Is Dangerous

What I realized from The New York Times strike is there are two different worlds when it comes to income expectations.

The first world of income expectations is based on a meritocracy. The better you do your job, the more you tend to get paid. If you stink it up, then your pay will rightly be less. If you feel you aren’t getting paid what you are worth, you leave.

The second world of income expectations is based on always getting paid more, no matter what. The economy may be in a recession, your company’s stock price could be in the dumps, a nuclear bomb may have detonated, yet you still think you deserve to get paid more.

This second view of getting paid violates the second rule of financial independence. Having this entitlement mindset is dangerous.

Eliminate Entitlement Mentality If You Want To Get Richer

Here are examples of how entitlement can hurt your wealth and happiness.

You study for one hour for the final exam while your peers average studying for three hours. Your peers get A’s and you get a B. You’re pissed because colleges reject you, but not them. You start questioning why life isn’t fair and end up a lonely, spiteful person. Screw the rich for having it so good!

Three years out of college, you expect to go to the corner office. When you get passed over for a promotion, you start bad-mouthing your colleagues and undermining your boss. You think, do you know who I am?! You turn into a virus nobody likes. As a result, your career trajectory derails.

The New York Times workers went on strike for a guaranteed 5.25% annual pay increase for four consecutive years. Yes, I understand everybody wants more money for the work they do. It’s always good to fight for what you think you deserve.

But maybe the strikers are misguided given they are working in the private sector where profits matter more than in the public sector.

The Demand To Make More In A Bear Market

2022 was the year of a recession and a bear market. With the way the Fed is raising rates, we will likely go into another recession by year-end 2023. More than a million jobs will likely be lost.

Wall Street strategists expect no gains in 2023 for the S&P 500. More importantly, The New York Times stock price (NYT) is at a three-year low!

How is expecting a guaranteed 5.25% annual pay increase in a struggling industry while inflation is heading down logical? Plenty of people in the media are losing their jobs. Instead of striking, perhaps it would be more rational to revert to 2019-level pay given NYT is back to 2019 levels.

After a couple rounds of layoffs in 2004, I dared not ask for my MBA tuition reimbursement one semester. Although it was a company benefit, to ask would have put my employment in jeopardy. So I sucked it up and paid the $12,500 out of pocket.

I know I might sound cruel, but eliminating entitlement is really for everyone’s own good. The sooner you can better align your expectations with the current realities, the sooner you can make optimal financial decisions.

Just because you are a certain race, work at a prestigious organization, or went to some elite university, doesn’t mean you automatically deserve to make more. You deserve to make more when you do great work AND when the economic conditions are right.

What Happened Once I Abolished Entitlement Mentality

After making one of the biggest financial mistakes at age 30, I had to suffer for the next 15 years with the consequences of overpaying. The Lake Tahoe property was my albatross that made vacationing less pleasant every time I went up.

At least I learned to never again expect my income to always go up. Here’s what else I did to help build more wealth:

Most importantly, I developed a strong money mindset that nobody was going to save me. As soon as I stopped expecting to always get paid and promoted, I began doing everything I could to generate alternative income streams. Real estate became my salvation. I sucked up the pain of managing property because I knew it was my main way to get free from working forever.

Held off on buying big ticket items I didn’t need. For example, I kept my old $8,000 Land Rover Discovery II for 10 years and traded it in for a Honda Fit that I drove for three years. I used the $80,000 I wanted to spend on a car in 2005 and invested it in the S&P 500.

Stayed consistent with Financial Samurai. Writing three posts a week for ten years is not easy. But Financial Samurai is an important financial buffer / insurance policy. If all my investments fail, at least I will have Financial Samurai spitting out pennies.

Expect Nothing And Get Richer As A Result

The ideal situation is if you can negotiate guaranteed income raises and pretend like you have no safety net.

Do you know why millions of Americans didn’t bother saving for retirement in the 1980s? Because they expected their company pensions to take care of them.

But then some companies went bankrupt and pensions disappeared or had shortfalls. As a result, many of these Americans ended up less wealthy than workers who never had a pension.

If you expect your 401(k) will be enough for retirement, you won’t build a taxable portfolio to generate passive income. Even worse, if you expect Social Security to cover all your retirement needs, you might not end up saving and investing at all!

Please get in the habit of expecting little-to-nothing. If you expect nothing, then everything is upside. When everything is upside, you will feel happier and richer as a result.

Keep fighting for the pay and promotion you think you deserve. Just be aware of the current realities. If you can avoid the biggest financial mistakes, you will likely end up much wealthier than those who do not.

Reader Questions And Suggestions

Readers, do you work at a private sector job where you always expect to get paid more, no matter how the company is performing? What other private sector jobs offer guaranteed pay raises?

Pick up a copy of Buy This, Not That, my an instant Wall Street Journal bestseller. The book helps you make more optimal investing decisions so you can live a better, more fulfilling life.

If you’re looking for a great retirement planning tool, check out NewRetirement. NewRetirement was built specifically for retirement planning and helping you stay retired.

For more nuanced personal finance content, join 55,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Job security is always a concern when choosing a career, but some fields are more recession-proof than others. And while there’s no guarantee that any job will be immune to cutbacks or layoffs, some industries weather economic storms better than others.

One industry that tends to be recession-resistant is finance. After all, people will always need financial services, whether investing their money, taking out loans, or managing their taxes. And while the finance industry has seen its share of ups and downs over the years, it generally bounces back fairly quickly after a downturn.

If you’re considering a career in finance, you’re probably wondering what the best-paying jobs are. With this in mind, we’ve compiled a list of the highest-paying finance jobs for 2023.

12 Highest Paying Jobs in Finance

While many finance jobs pay well, the following 12 positions sit at or near the top of the pay scale in 2023:

1. Chief Financial Officer

Average salary: $314,481 per year

As a financial executive, the chief financial officer (CFO) is responsible for the financial health of an organization. The CFO role is multi-faceted and includes everything from financial planning and analysis to business budgeting, financial decision-making, and risk management. CFOs typically have a deep understanding of economic theory and practice and strong analytical and problem-solving skills.

CFOs are some of the highest-paid finance professionals because they have experience and networks and excel at financial leadership.

2. Financial Manager

Average salary: $134,180 per year

Out of all the finance jobs available to college graduates, financial managers are some of the highest-paying, with high demand for workers in this field. According to the U.S. Bureau of Labor Statistics, employment numbers for Financial Managers are expected to rise by 17% over the next decade, faster than the average for all occupations.

Financial managers are similar to personal financial advisors, except they monitor businesses’ financial well-being instead of individuals. Most financial managers have previous experience working in market analysis and forecasting positions similar to this one.

Financial managers are responsible for developing long-term financial plans, directing investment activities, and generating financial reports for their company. They may work in various industries, such as investment firms, accounting firms, banks, or the government.

Employment numbers for Financial Managers are expected to rise by 17% over the next decade, faster than the average for all occupations.

3. Chief Compliance Officer

Average salary: $114,832 per year

A chief compliance officer ensures financial institutions adhere to all applicable laws and regulations. To keep a business running smoothly and help avoid costly non-compliance fees, CCOs monitor company policy and compliance.

This can be a demanding job, as the financial sector is heavily regulated. But it can also be rewarding, both financially and professionally. Chief compliance officers often have a degree in finance, law, accounting, or business administration. They also have experience working in the financial industry, usually at a senior level.

4. Insurance Advisor

Average salary: $89,295 per year

An insurance advisor’s primary job is to help customers find the best insurance products for their short- and long-term needs. This covers all areas of insurance – from life and home/auto coverage to financial planning services.

But an insurance advisor’s responsibilities go beyond simply finding the right policy. They must also help customers understand their coverage, file claims, and manage their accounts. In short, they are financial planning counselors who help people protect their assets.

A Bachelor’s degree in finance or a related field is required, and a CFP(Certified Financial Planner) certification is preferred for insurance advisors.

5. Hedge Fund Manager

Average salary: $83,578 per year

Who doesn’t want to make a fortune by correctly predicting the stock market? Hedge fund managers do just that. A hedge fund is a type of investment fund that uses financial instruments to offset the risk of investments. Hedge fund managers use their knowledge of the financial markets to manage their investment objectives, liquidity, and risk.

Hedge fund managers typically have a degree in finance, programming, economics, quantitative finance, or business administration.

6. Financial Examiner

Average salary: $81,410 per year

The financial examiner is responsible for managing risk, ensuring compliance with laws and regulations, and verifying that banks have adequate liquidity to cover unexpected losses. Financial examiners typically earn high salaries and enjoy above-average growth prospects.

Financial examiners are the middlemen between finance and law. Overall, their primary focus is ensuring that companies comply with all regulations so that nothing is mismanaged.

A minimum of a bachelor’s degree is needed for this profession.

7. Personal Financial Advisor

Average salary: $74,055 per year

Financial advisors help people invest their money after learning about their financial goals. They also often guide major life events, like saving for retirement or a college education. Because much of an advisor’s job revolves around talking to clients and seeking new investment opportunities, excellent communication skills are essential in this role.

8. Senior Accountants

Average salary: $73,547 per year

Senior accountants are responsible for managing the financial records of their organization. This includes preparing financial statements, maintaining ledgers, and overseeing budgeting. Senior accountants typically have a bachelor’s degree in accounting or a related field, along with a Certified Public Accountant (CPA) or similar designation.

9. Investment Banker

Average salary: $72,133 per year

As per the name, investment banking is the industry that banks use to invest in other companies. Investment bankers work with clients(businesses or government groups) to identify their financial needs and offer investment products, like stocks and bonds, to help them achieve their goals.

This is a very high-pressure job that requires being able to think on your feet and make quick decisions. Investment bankers also need to be able to work long hours, as they often have to travel to meet with clients.

10. Financial Analyst

Average salary: $70,677 per year

If you’re excellent with numbers and have a background or interest in finance, working as a financial analyst may be the perfect job for you. Financial analysts aid businesses and individuals by providing advice about how to invest money wisely. They keep track of economic trends, help make decisions about investments, and calculate value and risks.

They assist financial institutions, such as banks and insurance companies, with customer buying decisions and identifying their overall needs.

11. Information Technology Auditor

Average salary: $59,676 per year

Information technology auditors ensure that financial institutions have adequate controls to protect their information assets. This includes everything from systems and databases to applications and networks. IT auditors typically have computer science, information systems, or accounting degrees.

IT auditors are responsible for conducting audits and should therefore be experts at this task, which may require financial institutions to appoint them.

12. Budget Analyst

Average salary: $53,690 per year

Budget analysts are important in keeping companies organized and compliant with regulations. They help businesses and individuals budget by evaluating their spending and finding ways to save money. Budgeting can be tricky, but budget analysts have the skills and knowledge to make it easy.

Budget analysts typically work in the government or for accounting firms.

Whether you’re looking to become a financial analyst or an investment banker, there are certain skills you’ll need to succeed in finance. These include:

Accounting Skills

What makes finance different from other business disciplines is its focus on numbers. Financial professionals need to be able to understand and interpret financial data. This requires strong accounting skills.

Management Skills

How you manage your own finances is one thing, but being able to manage the finances of an entire company is another. Financial managers are responsible for overseeing the financial operations of their organization. This requires strong management skills.

Analytical Thinking Skills

Employers need workers who can compile financial statements, but business leaders must be able to interpret and use this information to their advantage. This is referred to as financial statement analysis: a comprehensive review of key financial documents to assess a company’s effectiveness. This task requires strong analytical thinking skills.

Not only finance but every business discipline requires good analytical skills as employers always seek those who could think outside the box.

Communication Skills

Finance is a complex field, and communicating effectively is essential for success. Financial professionals need to be able to explain their ideas clearly and concisely. With so much at stake, there is no room for error when communicating with clients or business partners.

Financial Reporting Skills

Although it’s important to analyze past data, finance professionals know that looking forward is key to success. This is why financial reporting skills are essential. Financial reports give insights into a company’s current financial health and can predict future trends.

Thinking critically is of the utmost importance for business leaders when it comes time to make big decisions like hiring, budgeting, and strategic planning. Therefore, if you want your resume to stand out, including this skill is a must!

Financial Decision-Making Skills

Making decisions is key for anyone who wants to be a business leader. While leaders need to understand an organization’s goals and objectives, they also need to be able to make decisions that will help their company achieve these goals.

This requires an understanding of financial concepts and an ability to think creatively and develop innovative solutions. Finance decision-making is vital in determining whether or not a company will succeed.

These are key skills you’ll need to succeed in finance. If you have two or three of these skills, you’re on your way to a successful career in this exciting field.

The Benefits of a Career in Finance

Who knows, with a career in finance, you might even be able to retire early! But seriously, there are many benefits to pursuing a career in finance.

Some of the benefits of a career in finance include the following:

Huge Range of Roles and Job Security

As with any industry, various roles are available in finance. And because the financial sector is so important to the functioning of the economy, it’s safe to say that there will always be a demand for financial professionals.

This means your job is likely secure no matter what happens in the economy. And if you’re looking for a change, there are plenty of other roles you can pursue within the financial sector.

High Earning Potential

Never underestimate the earning potential of a career in finance! If you’re good at what you do, you can make a lot of money. Many finance professionals are among the highest-paid workers in the world.

Of course, your salary will depend on several factors, including your experience, education, and the company you work for. But if you’re looking to make a good living, a career in finance is worth considering.

Most Finance Professionals Are Highly Satisfied with Their Jobs

In an era of increased job dissatisfaction, it’s refreshing to know that some professions still offer high satisfaction levels. According to a Moster.com survey, finance is one of these professions.

While the survey is several years old, it found that finance professionals are some of the most satisfied workers in the world, with 36% of respondents saying they are satisfied with their jobs.

This is likely due to a finance career’s high earning potential and job security. Finance is worth considering if you’re looking for a stable and satisfying career.

Flexibility and Room for Growth

One of the great things about a career in finance is that it offers a lot of flexibility. There are many different types of finance jobs, so you can easily find one that suits your lifestyle.

And because the financial sector is always changing, there’s always room for growth in your career.

Is a Career In Finance Right for You?

Perhaps you’ve read through the list and wondered if a career in finance is right for you. Here’s a video to help you assess your skills and interests and decide on a career, whether it’s in finance or something else!

FAQs about Finance Careers

What is the hardest finance job?

There is no easy answer when it comes to the hardest finance job. It depends on your skillset and experience. Some people find investment banking, controllers, tax managers, and valuation analysts to be the most challenging, while others find corporate finance more difficult.

What is the least stressful finance job?

Accounting is often considered the least stressful finance job. This is because it generally doesn’t involve as much pressure as other finance roles.

What is the highest-paid job in finance?

Chief Executive Officers such as chief financial officers (CFOs) oversee the entire company and have high salaries. The CFO primarily controls financial affairs.

Why do finance jobs pay so well?

There are a few reasons why finance jobs pay so well. First, finance is a very important sector of the economy, and those working in finance are responsible for ensuring that businesses and individuals have the capital they need to succeed.

Second, finance is a highly specialized field, and those who work in finance have spent years studying and training for their careers.

Finally, finance jobs are often very demanding, and those who work in finance are often willing to work long hours to finish the job.

The Bottom Line: Is a Career in Finance Worth It You?

A finance degree is valuable to students. Entry-level finance majors earn an average of $55,000 a month. Compared to mid-career salaries, they are about 101,000 a month.

According to the Bureau of Labor Statistics Occupational Outlook Handbook, this is remarkably higher than the median annual wage of $45,760 in the USA. In other words, finance majors make a lot of money. And that isn’t the path for you, you can always consider these self-employed job ideas.

Preferred shares are complicated investments only suitable for knowledgeable investors

Most people invest in preferred shares for the tax-efficient dividend income.Photo by Getty Images/iStockphoto

Article content

In an increasingly complex world, the Financial Post should be the first place you look for answers. Our FP Answers initiative puts readers in the driver’s seat: you submit questions and our reporters find answers not just for you, but for all our readers. Today, we answer a question from Elmar about preferred shares.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

Article content

By clicking on the sign up button you consent to receive the above newsletter from Postmedia Network Inc. You may unsubscribe any time by clicking on the unsubscribe link at the bottom of our emails or any newsletter. Postmedia Network Inc. | 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of FP Investor will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

By Julie Cazzin with Allan Norman

Q: I am heavily invested in preferred shares. Is it right to stay there in today’s market? Or should I seek out different investments? — Elmar

FP Answers: Elmar, if you are an experienced preferred-share investor, then you know you’ve given me a difficult question to answer with the limited information you’ve provided. What type of preferred shares are you holding: retractable, rate reset, perpetual, fixed floating or floating rate?

Probably the best way for me to answer your question is to explain why I think people invest in preferred shares, give a brief description, provide an example of what I think you’re seeing on your investment statement, and then discuss your options based on the example.

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

I suspect most people invest in preferred shares for the tax-efficient dividend income. It’s generally higher than guaranteed investment certificate (GIC) or bond income, and there is a perceived safety in owning preferred over common shares.

Preferred shares are equity investments that pay a fixed dividend, but they don’t share in the growth of the issuing company like common shares do. If the issuing company goes bankrupt, bond holders will be paid out first, followed by preferred shareholders and then common shareholders. In reality, I doubt preferred shareholders will receive anything if the issuing company goes bankrupt.

The share value of a preferred share will rise and fall with changes in interest rates, similar to a bond. Share value goes down when interest rates go up, and share value goes up when interest rates go down. Unlike bonds, there is no maturity date, so the dividend payments in most cases never end, unless the issuing company calls to redeem the preferred share or goes bankrupt.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

The issuing company will most likely redeem a preferred share when it is in their best interest to do so. This may happen when a new preferred share can be issued at a lower dividend rate than the current rate.

Rate-reset preferred shares are the most common type of preferred shares in Canada and the accompanying table shows a real example of what a rate-reset preferred share may look like on an investment statement right now:

The table tells you a few things: the dividend rate at issue, or at last reset, was 4.57 per cent; if sold today, the capital loss would be $8,727 (book value minus market value); and the current yield is 6.08 per cent, or annual dividend payments of $1,395 ($22,950 times 6.08 per cent).

Elmar, based on what’s presented in the table, should you hold or sell this preferred share? It depends on how you like to invest, your goals, when you need the money and other factors, coupled with some future unknowns such as changing interest rates.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

If you hold, you will continue to collect the dividends even though the share value is down. It isn’t too different from having a rental property drop in value while the rental income continues. In the case of a rental property, you likely wouldn’t sell the rental if your primary goal is income, or you would wait until the property went back up in value before selling.

If interest rates continue to go up, the value of the preferred share is likely to go down. However, there will be a rate reset in 2024 based on the five-year Bank of Canada bond yield plus a spread. Under that scenario, you will receive a higher dividend payment in 2024.

Ideally, once the new dividend rate has been set in 2024, interest rates will start to fall, causing your share price to rise. The catch is, if interest rates fall too much, the issuing company may redeem the shares at the issue price. This is why preferred shares have limited upside potential, but that may not be a concern to income-oriented investors.

Advertisement 6