2023 housing price forecasts from various institutions range from -22% to + 5.4%. There is no consensus as to which way house prices will go. However, the bias is towards the downside.

There is also the issue of forecasting the national median home price and the price of your local housing market. While we care about the national median home price forecast, we care way more about our local housing market forecast.

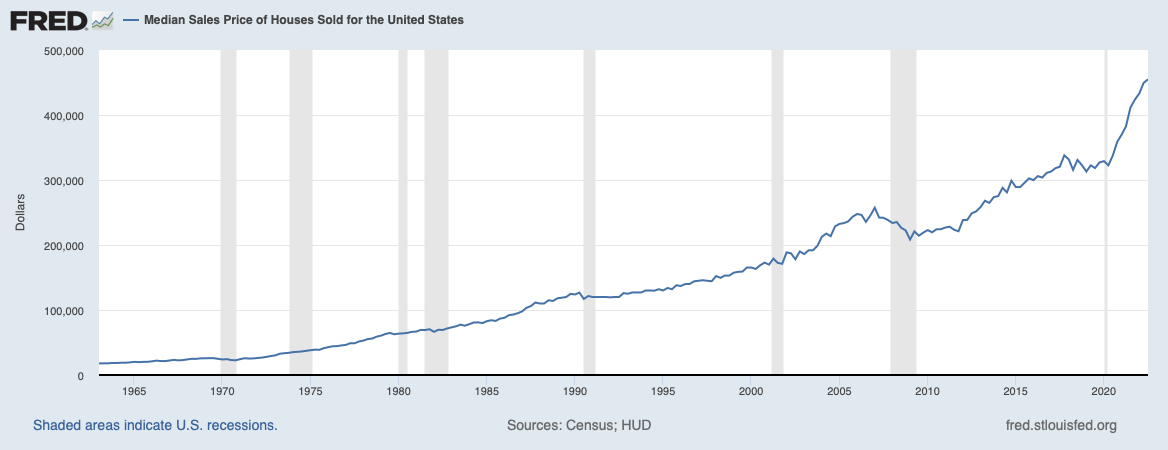

For background, I expected the median sales price in the United States to rise by 8% to 10% in 2022. My estimate was less bullish than the majority of firms expecting 15% – 18% price increases.

The 4Q2021 median home price was $423,600. The latest pricing data available, 3Q 2022, shows the median home price of $454,900, or a 7.4% increase. 4Q 2022 housing price data will be released in 1Q 2023.

2023 Housing Price Forecasts

Take a look at the housing price forecasts for 2023 from some popular real estate or real estate-related institutions. They are all over the place!

The Most Bearish Housing Forecasts For 2023

John Burns Real Estate Consulting (JBREC): -20% to -22%

Zonda: -10%

Goldman Sachs: -5% to -10%

Redfin: -4%

The Most Bullish Housing Price Forecasts For 2023

Realtor.com: +5.4%

CoreLogic: +4.1%

National Association Of Realtors: +1.2%

The Most Boring Housing Price Forecasts For 2023

Fannie Mae: -1.5%

Freddie Mac: -0.2%

MBA: +0.7%

Zillow: +0.8%

My Thoughts On The Extreme Housing Price Forecasts

When it comes to forecasting, it’s good to first look at the tail ends. It helps to see who is delusional and whether you have any blind spots.

Most Bearish Call

I like the work of John Burns Real Estate Consulting (JBREC). However, they are too pessimistic forecasting a -20% to -22% decline in housing prices in 2023. A 20% median home price decline would bring the national median home price down to about $364,000.

A 20% – 22% price decline would mean a GREATER decline than the one during the global financial crisis. Median home prices declined from $257,000 in 1Q 2007 to $208,400 in 1Q 2009, or -18.9%. Further, it took two years for national median home prices to decline by 18.9%.

It is improbable the national median home price will decline by more than it did during the global financial crisis in half the amount of time.

If we say this housing downturn is 30% as bad as the one from 2007 – 2009, then we’d get to a -5.7% housing price decline.

Most Bullish Call

On the flip side, there’s the +5.4% housing price forecast by Realtor dot com. Realtor dot com is a website that helps you find a realtor to buy or sell a home. The realtor pays a referral fee on closed transactions. The stronger the housing market, the more business Realtor dot com will generate.

It’s not a coincidence CoreLogic (+4.1%),the National Association Of Realtors (+1.2%), Mortgage Bankers Association (+0.7%), and Zillow (+0.8%) are all also looking for higher median house prices in 2023.

With a Fed-induced recession likely in 2023 and higher average mortgage rates, I think every forecast that shows an increase in 2023 housing prices is wrong.

My 2023 Housing Price Forecast

With an 75% conviction level, I expect the median housing price for 2023 to decline by 8% to $418,000. I’m assuming the median house price ends 2022 at $455,000.

The reasons include:

- A global recession by the end of 2023

- The Fed insisting on hiking to a 5% – 5.125% terminal rate even though inflation is clearly declining and annualizing under 2%

- A higher risk-free rate makes investing in risk assets less appealing

An 8% decline in housing prices is disappointing for real estate owners. However, real estate has outperformed the S&P 500 by over 25% in 2022. Giving back 8% is not that bad, especially if you bought responsibility or have little-to-no mortgage left.

The reasons why I don’t expect home prices to decline by more than 8% are:

- 30-year fixed mortgage rates should decline by 2% – 3% from their peak of 7% by mid-2023. 4% – 5% 30-year fixed mortgage rates should bring back demand.

- The Treasury bond market has stopped listening to the Fed. The 10-year bond yield did not move after the Fed raised rates another 50 bps on December 14, 2022. The huge yield inversion between the 10-year and the 3-month Treasury bond is saying the Fed is making a mistake. And retail mortgage rates are priced largely off the 10-year bond yield.

- Consumers still have “excess” savings thanks to tremendous stimulus spending in 2020 and 2021.

- There will continue to be an undersupply of homes. The vast majority of homeowners have 30-year fixed mortgage rates under 5%. Therefore, there’s no need for most to sell.

- The will be a continued capital shift towards real assets and away from funny money assets like stocks, cryptocurrencies, and anything else that provides zero utility.

Downside Risks To My Negative Housing Price Forecast: Desperation

One of the biggest unknowns is how much new housing supply will come to market during the traditionally strong spring season. If there are too many desperate sellers, we could see home prices fall by more than 8% .

You also have funky scenarios where a house is priced too high and becomes “stale fish.” You might also encounter extremely motivated sellers going through a divorce. One short-sale can ruin the values of a dozen neighboring homes.

The other main downside risk to my negative housing price forecast is a more aggressive Fed. Although the Treasury bond market has stopped believing the Fed, a 5.125% Fed Funds rate will squeeze consumer debt borrowers. Everything from credit card rates to auto loan rates will go up.

A minority of thinly stretched borrowers can cause harm to the majority who have their finances in order.

Seeing prices fall by 8%+ in your local housing market is easy to see, especially if your housing market showed the most robust gains in 2020 and 2021. Prices in Boise and Austin could easily fall by 20% from their peaks before bottoming.

Biggest Upside Risk To My Negative Housing Price Forecast: Stealth Wealth

I may be underestimating the amount of liquid wealth potential buyers are holding. The amount of stealth wealth out there is more than we all know. Further, I may also be underestimating how much demand will return to the housing market if mortgage rates do decline by 2% – 3% in 2023.

Personally, I have a lot of cash and short-term Treasury bonds. So do all of my friends. I have a feeling, many Financial Samurai readers have an elevated amount of cash as well.

If many of us are going to be hunting for housing deals in 2023, will housing prices really decline by my forecasted 8%? Maybe not. I still believe house prices will decline, but perhaps by only 5% instead.

When it comes to housing prices, prices tend to get bid up quicker than they fall. Hence, buyers might only have a short window to take advantage of price discounts.

Mortgage Demand Highly Sensitive To Even High Rates

Take a look at this chart below. It shows a surge in mortgage purchase applications as the average 30-year fixed rate fell from 7.1% in October 2022 to 6.3%. 6.3% is still high compared to a year ago. But mortgage purchase applications went up 13.8%.

Hence, if mortgage rates fall to 4% – 5% by mid-2023, perhaps we will see a 25%+ increase in mortgage purchase applications. The longer the inactivity in real estate transactions, the greater the pent-up demand.

There Will Always Be Opportunities

Real estate continues to be my favorite asset class to build wealth for most people.

Even if all my properties decline by 10% on average in 2023, I don’t care because I don’t feel it. I will continue to raise my family in our primary residence. Then I’ll continue to collect my rental income to help pay for our lifestyles.

An asset that provides both income and utility is the best type of asset class to own. However, tenant headaches, maintenance issues, and property taxes can get to even the most patient real estate investors. As a result, a diversification of investments into stocks, real estate, bonds, and alternatives is recommended.

If you want to buy real estate in 2023, there will be plenty of opportunities to do so at more reasonable prices. The combination of declines in both housing prices and mortgage rates will make real estate more attractive by the middle of 2023.

When that time comes, I just hope nobody bids against me. Being able to buy my current forever home once lockdowns began on March 18, 2020 was ideal. If I had faced competition, I would have easily paid 4% more.

Reader Questions And Suggestions

Readers, what are your housing price forecasts for 2023 and why? Are you planning on hunting for deals in 2023? What would cause you to sell your property in 2023?

If you want to invest in real estate more surgically, take a look at Fundrise. Fundrise primarily investments in single-family and multi-family homes in the Sunbelt. Its income fund is generating an 8%+ yield. Further, Fundrise is using its existing cash to hunt for distressed deals with 13-14% yields. I just spoke to Ben Miller, the CEO for an hour.

Pick up a copy of Buy This, Not That, my an instant Wall Street Journal bestseller. The book helps you make more optimal investing decisions so you can live a better, more fulfilling life.

For more nuanced personal finance content, join 55,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.